Key Takeaways

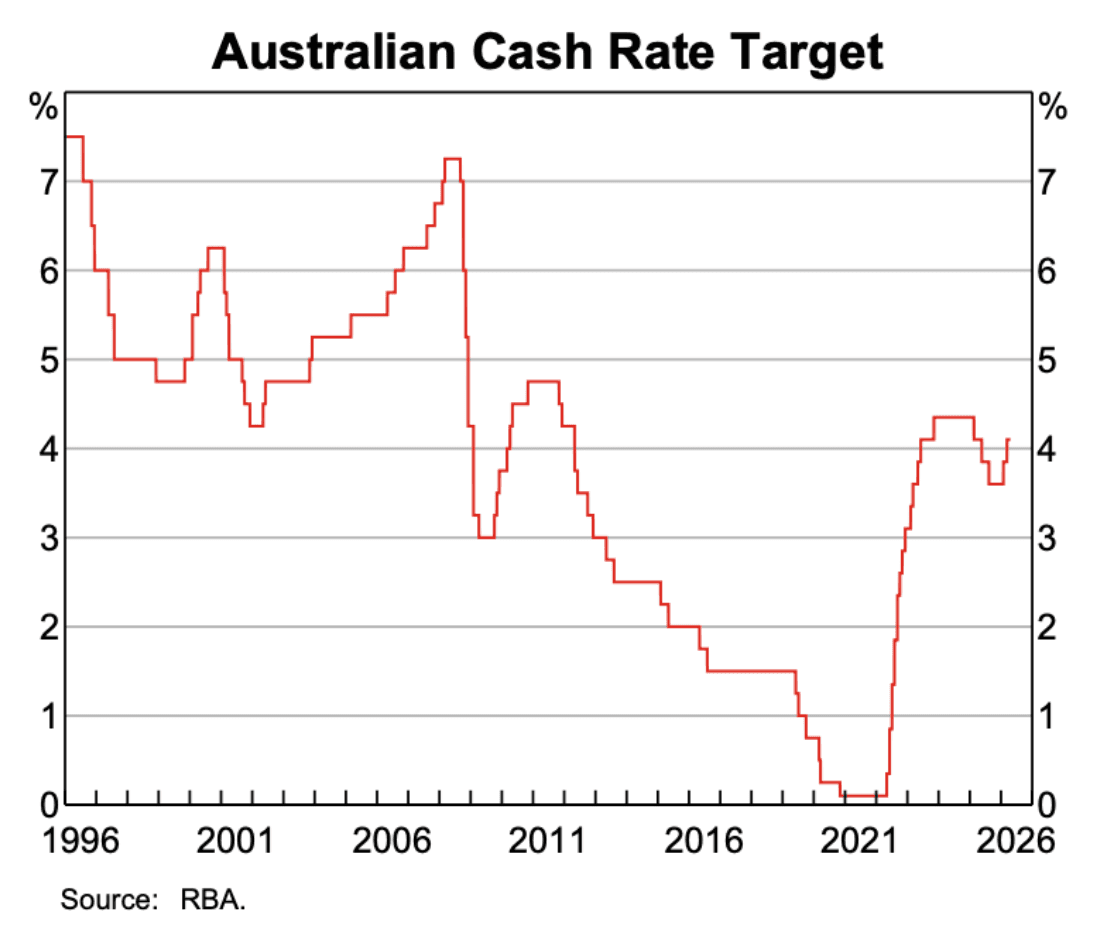

The RBA has raised the cash rate 25bp to 4.35% — the third hike of 2026 with rates now back at the prior cycle peak in early 2024.

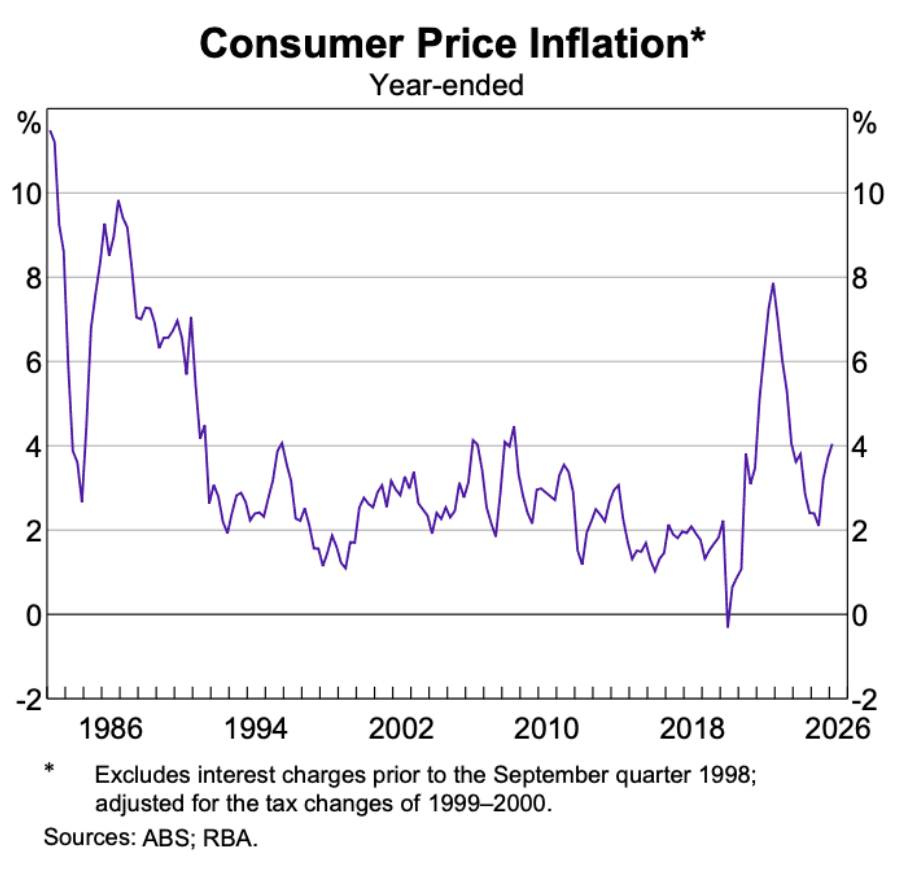

Inflation remains the driving force: headline CPI hit 4.6% in March, its highest since 2023, while underlying inflation (trimmed mean) held at 3.3% — above the RBA's 2–3% target.

Markets are pricing in at least one further hike later in 2026, with the next inflation data due in late May.

In an elevated-inflation, positive-growth environment, real assets like gold and commodities, and inflation-linked bonds, may offer portfolio resilience alongside traditional equities. For what a stronger AUD means for your portfolio, see our recent piece.

Coming up next week on May 12 is the Federal Budget, the next key economic event for investors.

This week, the Reserve Bank of Australia lifted the cash rate by 25 basis points, moving from 4.10% to 4.35%. It is the third consecutive rate increase of 2026, following hikes in February and March that together reversed nearly all of the easing delivered across 2025. At 4.35%, the cash rate is back at its prior cycle peak seen in early 2024.

The decision was near unanimous with 8 of 9 Board members voting in favour of the hike. While economic growth and a tight labour market have held up, headline inflation has re-accelerated, driven in part by global factors like energy prices. The Board noted that their outlook for inflation has been revised higher while economic conditions are more uncertain compared to their prior meeting. This highlights the difficult balancing act the RBA faces, weighing persistent inflation against the impact of further rate rises on households and the economy. They currently forecast approximately one additional hike in their forward-looking forecasts of the cash rate for 2026.

Markets are pricing in at least one further 25 basis point increase later in the year, according to the ASX interbank futures — likely during the September or October meeting. An additional 25bps hike move would take the cash rate to 4.60%.

What Does This Tell Us About the Economy?

The decision to hike for a third consecutive time reflects inflation running hotter than the RBA is comfortable with — and a picture that has grown considerably more complicated since the start of the year.

Growth has been resilient – GDP expanded in the December quarter 2025, rising above the RBA's own estimates of the economy's potential growth rate and survey measures of capacity utilisation confirmed that the demand carried into early 2026. The labour market has remained tight, with unemployment holding at 4.3% in March.

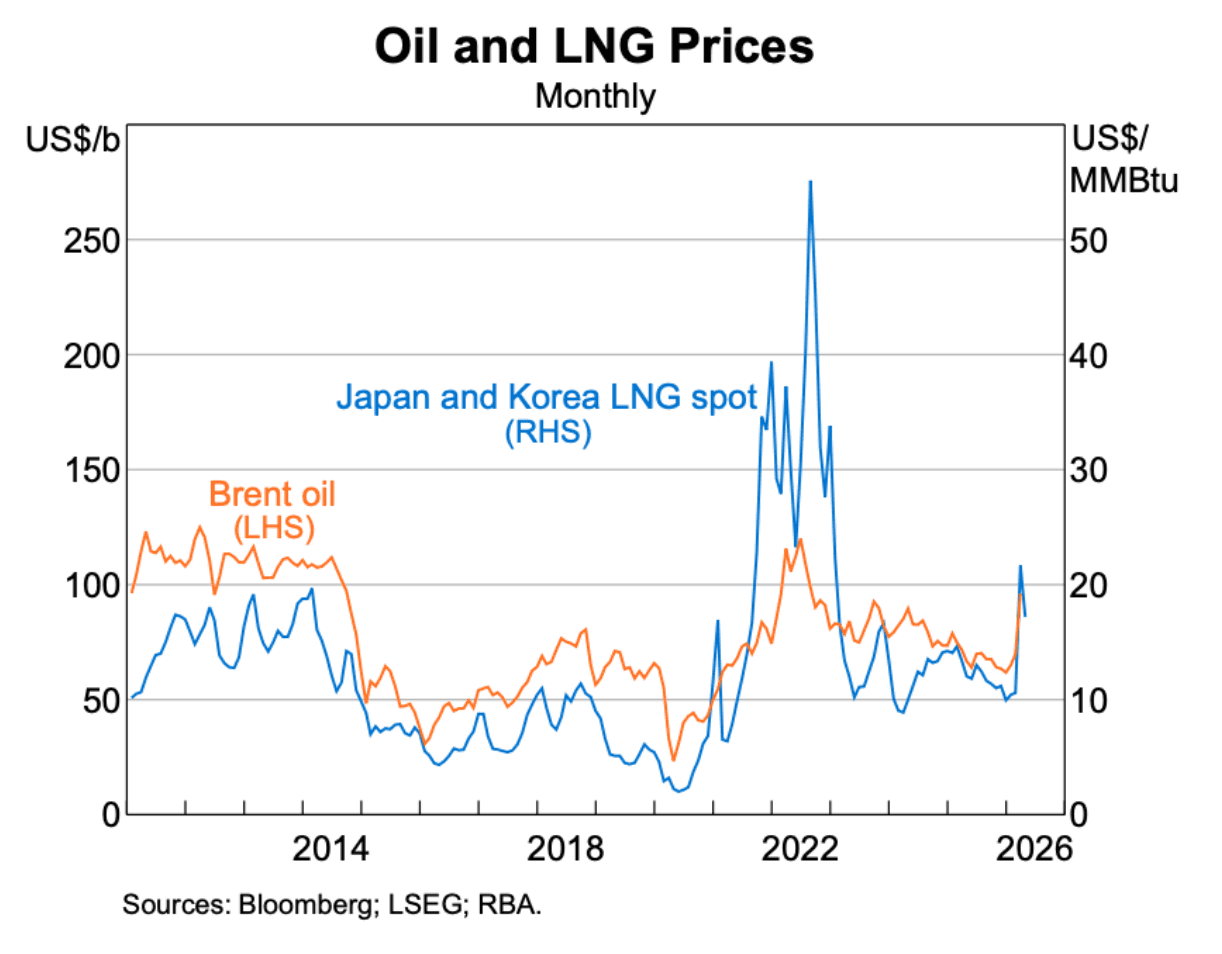

Inflation, however, has become a more urgent problem than the RBA anticipated even three months ago. Headline CPI jumped to 4.6% in the year to March 2026 — driven in part by a sharp rise in fuel prices following the outbreak of conflict in the Middle East. The RBA's preferred underlying measure, the trimmed mean, came in at 3.3% for the year to March — still above the 2–3% target band, though the quarterly outcome was slightly softer than expected, offering modest reassurance that domestic price pressures are not re-accelerating on their own.

Going into the May meeting, the RBA's projections had headline inflation peaking at around 4.2% by mid-2026. The conflict changed that. The revised baseline now puts the headline peak at 4.8% in mid-2026, with underlying inflation remaining above 3% until late 2027.

Beyond the direct hit from fuel, the RBA flagged that higher energy costs are already showing signs of passing through to the prices of goods and services more broadly — so-called second-round effects. This is a key reason the Board felt it could not simply look through the inflation spike as a temporary overseas shock.

Where Do Rates Go From Here?

Three hikes in quick succession represent a meaningful tightening for the Australian economy. Cumulative impacts on variable-rate borrowers take time to fully flow through. While the trimmed mean inflation is not accelerating in recent data, oil prices have remained elevated.

The case for further action rests on the fact that underlying inflation remains above target, that the labour market is still tight, and that financial conditions — despite three hikes — have not yet been too restrictive. However, the board's Statement noted that there is more uncertainty on the economy outlook and the rise in energy prices and interest rates may lower future spending. In summary the RBA’s outlook for inflation is now higher and outlook for growth lower than it previously expected. This highlights the difficult balancing act the RBA faces, weighing persistent inflation against the impact of further rate rises on households and the economy.

The key data points that will decide the next meeting are:

Monthly CPI data (due in late May): If the trimmed mean begins to fall toward 3%, the case for a pause strengthens considerably. If it ticks up, July or August rate hikes become a real possibility.

Labour market prints: Unexpected softness in employment would shift the balance toward a hold (May 21 and June 25 are the next reports).

Global energy prices: A de-escalation in the Middle East conflict that brings fuel costs lower would reduce headline inflation quickly and potentially give the RBA room to wait and hold.

The May 12 Federal Budget (see below): Government spending decisions are more long term in nature but will feed directly into the RBA's demand and inflation forecasts for how much stimulus is being provided from government spending.

While further rate hikes could be on the cards in the remainder of the year, a rate cut this year seems unlikely unless there is a big shift in global energy prices and economic growth outlook.

What This Means for Asset Prices

The immediate market response to the decision was relatively muted with the market having priced in a high likelihood of a rate hike. The ASX 200 was relatively muted in performance over the past month, potentially indicating some of the rate-sensitivity repricing had occurred in advance. Looking further ahead, the environment created by elevated inflation alongside moderating growth is a nuanced one.

Economic environments where inflation is elevated but growth is still positive have historically been supportive of risk assets like equities, particularly those with pricing power and exposure to commodities.

Financials (banks) are a relative beneficiary of higher rates over time, as net interest margins expand when lending rates rise faster than deposit costs. The three major-bank dividend payers — CBA, NAB, ANZ, Westpac — are now operating in a structurally higher-margin environment. The risk to monitor is credit quality: three hikes in short order increase pressure on over-leveraged borrowers, especially in housing markets.

ASX: MVB – VanEck Australian Banks ETF

VanEck's MVB ETF holds only Australian bank stocks, concentrated in the Big Four.ASX: QFN – BetaShares Australian Financials Sector ETF

QFN by BetaShares BetaShares' ETF covers the broader Australian financials sector, including banks, insurers, and diversified financials.

REITs face the most direct headwinds. Higher discount rates compress asset valuations, refinancing costs rise, and income distributions become less competitive relative to risk-free alternatives.

ASX: VAP – Vanguard Australian Property Securities Index ETF

VAP by Vanguard tracks Australian listed property securities and REITs.

Resources and energy names tend to hold up comparatively well: the same geopolitical forces driving inflation are supporting commodity prices and a tailwind for Australian energy producers.

ASX: QRE

BetaShares' QRE ETF focuses solely on Australian resources and mining companies.ASX: OZR

State Street's SPDR OZR ETF tracks the S&P/ASX 200 Resources Index, holding only the largest Australian energy and mining companies like BHP, Rio Tinto, and Woodside.

However, if the growth picture deteriorates — if three hikes prove to be too much and consumption falls more sharply than expected while energy-driven inflation stays persistent — then investors face a more challenging environment. In that scenario, two asset classes warrant particular attention:

Inflation-linked bonds provide a direct hedge against persistent price rises. Unlike nominal bonds, their principal and interest payments are indexed to inflation, meaning they preserve purchasing power when inflation stays elevated. For investors concerned that the RBA is fighting an inflation problem from overseas forces that it cannot fully resolve with rate hikes, inflation-linked bond exposure can act as a counterweight to the rate sensitivity that sits elsewhere in a portfolio.

ASX: ILB

BlackRock's ILB ETF holds Australian government inflation-linked bonds, with returns tied to CPI.

Real assets — gold and commodities — have often attracted investor attention in uncertain economic environments. Gold and commodity-linked ETFs offer exposure to these asset classes such as ETFs such as:

ASX: QAU

BetaShares' QAU ETF tracks physical gold bullion, hedged back to AUD.ASX: QCB

BetaShares' QCB ETF provides diversified exposure across energy, metals, and agricultural commodities, hedged to AUD.ASX: GHLD

Global X's GHLD ETF tracks physical gold bullion, also hedged back to AUD.

Next Watchpoint: The Federal Budget, 12 May 2026

Next week, Treasurer Jim Chalmers will hand down the 2026–27 Federal Budget — the Albanese government's first since winning the May 2025 election.

The Budget is expected to include a productivity package and savings measures. Cost-of-living relief measures are anticipated — potentially including an extension of the fuel excise cut. There is also speculation around changes to the capital gains tax concessions (including negative gearing), an important watching point for investors.

From a monetary policy perspective, the key question is whether the Budget adds stimulus or restraint to an economy the RBA is actively hiking rates to temper inflation. A budget that increases demand will complicate the RBA's job and could make further rate hikes more likely. A fiscally disciplined budget may give the board room to pause.

Important disclaimer: SelfWealth Pty Ltd ABN 52 154 324 428 (“Selfwealth”) (AFSL 421789). The information contained on this website is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser and/or accountant. Taxation, legal and other matters referred to on this website are of a general nature only and should not be relied upon in place of appropriate professional advice. You should obtain the relevant Product Disclosure Statement for any product mentioned and consider its contents before making any decision.

Most Recent Articles