Meanwhile, equity markets are hitting all-time highs, seemingly unbothered by the tightening rates around them. It's the kind of divergence that typically precedes a turning point.

We break down the tension between bonds and stocks, where the RBA goes from here, and the investing opportunities hiding in plain sight.

Key Takeaways

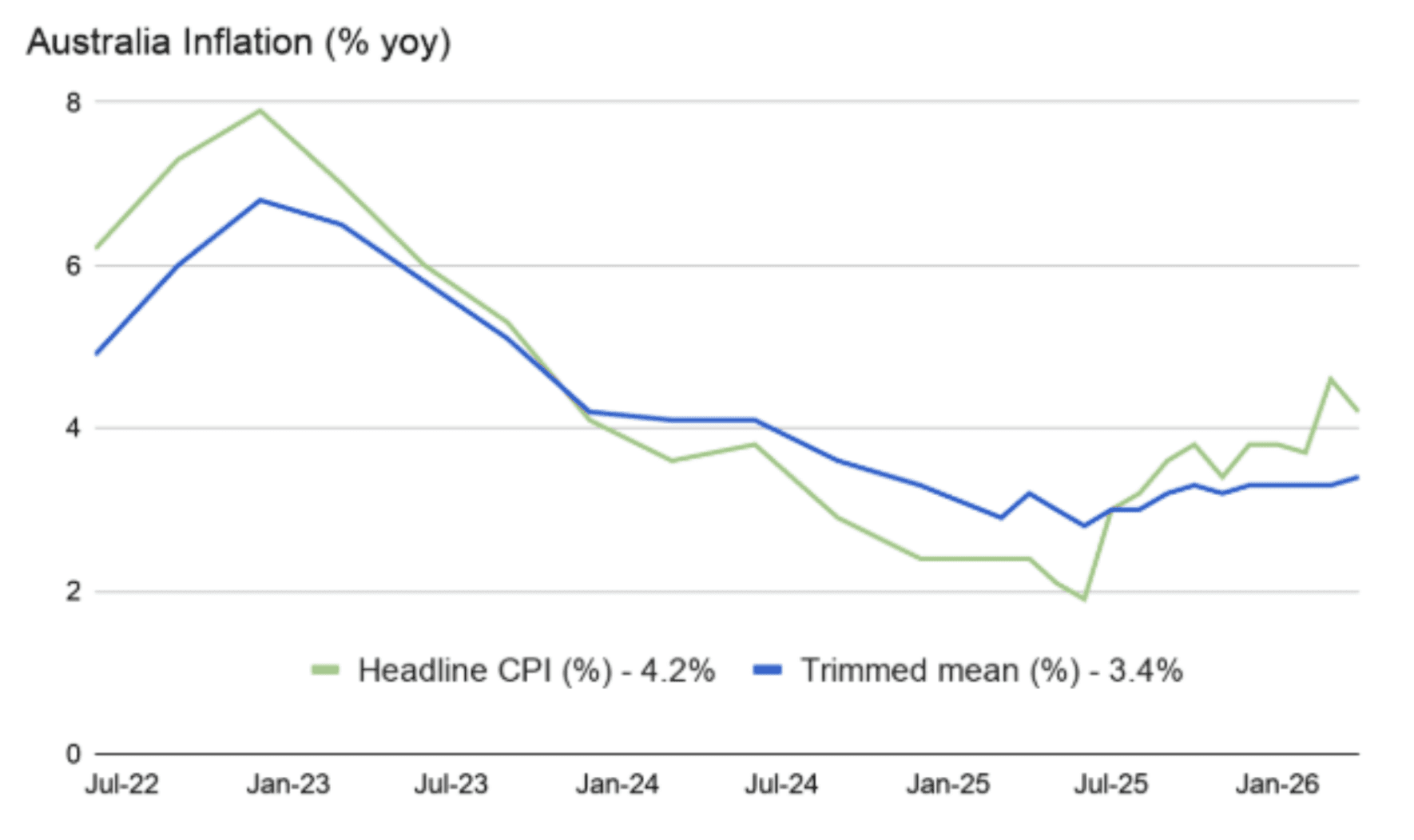

Australia's monthly CPI for April came in at 4.2%, down from 4.6% — but the trimmed mean remains at 3.4%, still above the RBA's 2–3% target band

The result likely keeps the RBA on hold; the Board needs sustained progress before moving in either direction

Bond yields are at multi-year highs — income investors have a window to lock in attractive rates

US and Asian equity markets are surging to record highs on strong earnings, easing political tensions, and positive semiconductor sentiment

Next key data: Australia Q1 GDP (June 3) and US jobs data (June 5)

Australian Inflation: Holding, Not Healing

April's monthly CPI reading of 4.2% — down from 4.6% — will be welcomed, but it isn't the breakthrough the RBA is looking for. The trimmed mean, the Board's preferred gauge of underlying inflation, held at 3.4% for the year. That keeps it firmly above the 2–3% target band. Progress, but not enough.

Energy costs remain the biggest driver of headline inflation — a global problem as much as a domestic one, though some easing in fuel prices over the past month provided modest relief. Encouragingly, domestic inflationary pressures aren't accelerating, and the labour market showed early signs of softening with unemployment ticking up to 4.5% from 4.3%.

Three consecutive rate hikes — in February, March, and May — have lifted the cash rate to 4.35%. This week's result doesn't give the RBA reason to move again at the next meeting, but it's equally not the all-clear to begin cutting. Markets are still pricing in a possible further hike in September or October, but that remains far from certain. For now, the Board watches and waits.

The Global Picture: Rates Rise, Markets Shrug

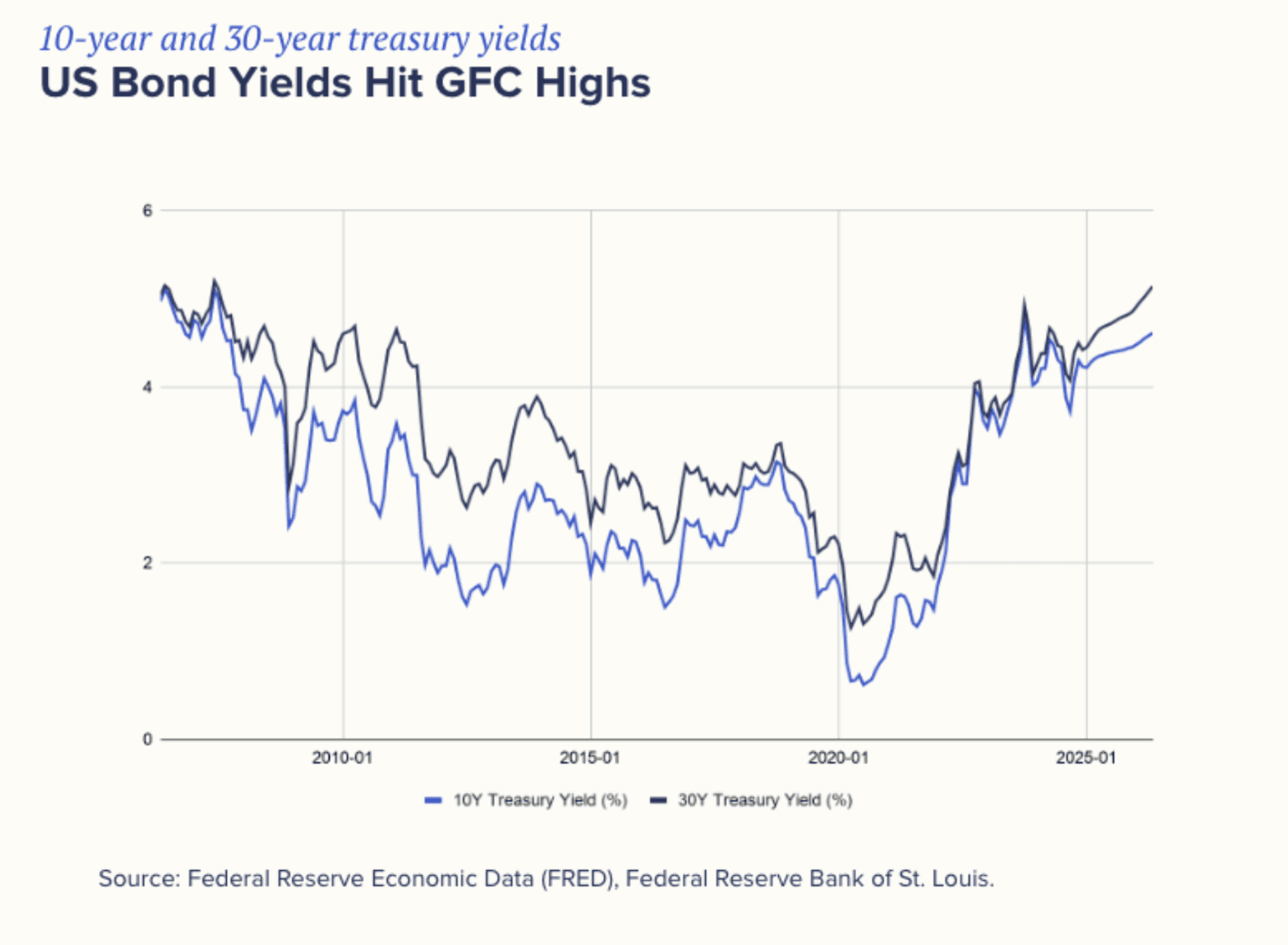

Globally, inflation isn't going quietly. The Iran War continues to disrupt supply chains and keep energy prices elevated. US April headline CPI came in at 3.8% year-on-year — the highest since May 2023 — and markets have rapidly repriced US rate expectations: from two cuts priced in at the start of 2026, the market is now approaching pricing in one hike by January 2027.

That repricing pushed US 10-year Treasury yields briefly to 4.6% and 30-year yields above 5% — levels not seen since the Global Financial Crisis. Australian 10-year yields have been more stable around 5%, reflecting the RBA's head start on the hiking cycle.

And yet equities are surging. The S&P 500 closed at a record 7,519.12 on Tuesday. The Nasdaq, Taiwan, and South Korea — all tech and semiconductor-heavy — are posting historic highs. Nvidia delivered another blockbuster quarter. Earnings are carrying the market even as the rate environment tightens around it.

What It Means for investors

Bond and equity markets are sending conflicting signals. Fixed income is flagging inflation concern and the possibility of further hikes; equities are pricing in an optimistic earnings outlook. Both can be right — for now.

The tension worth watching: when US 10-year yields cross 4.5%, Treasuries start offering a genuinely competitive alternative to equities. When borrowing costs exceed the economy's long-run growth rate — as they do today — that's historically been a headwind for stocks. It doesn't always end the rally, but it narrows the margin for error.

For income investors, the current environment is one of the more attractive entry points in years. Australian government bond yields at multi-year highs offer a meaningful real return. Investors who lock in longer-duration bonds today may benefit from both the income and potential capital gains if yields eventually fall. Shorter-dated instruments — term deposits, high-interest savings accounts — are attractive now but could reprice quickly once the rate cycle turns.

Fixed Income ETFs to consider:

ASX: IAF — iShares Core Composite Bond ETF. Broad Australian investment-grade exposure; a core fixed income holding

ASX: ILB — iShares Government Inflation-Linked Bond ETF. Principal adjusts with CPI — a direct hedge if inflation proves stickier than expected

ASX: FLOT — VanEck Investment Grade Floating Rate ETF. Provides exposure to investment-grade floating rate bonds, with income that adjusts as interest rates move — offering capital stability with rate-sensitive income in the current environment.

ASX: QPON — BetaShares Australian Bank Senior Floating Rate Bond ETF. Floating rate income that doesn't reprice lower immediately if the RBA stays on hold

ASX: VAF — Vanguard Australian Fixed Interest Index ETF. Low-cost, diversified exposure to Australian government and investment-grade corporate bonds

ASX: GBND — BetaShares Sustainability Leaders Diversified Bond ETF (Currency Hedged). For investors seeking global fixed income exposure with an ESG overlay and AUD hedging

Australian Equities & Resources:

The same geopolitical dynamics keeping inflation elevated are supporting commodity prices and Australia's LNG producers. The structural energy security theme — governments diversifying supply chains, AI driving surging data centre power demand — remains intact. As noted in our recent piece, ASX Materials and Energy have been the standout sector performers in 2026. The key risk: a rapid resolution in the Middle East could deflate commodity prices faster than markets expect.

ASX: OZR — SPDR S&P/ASX 200 Resources ETF. Holds BHP, Rio Tinto, Woodside and peers

ASX: QRE — BetaShares Australian Resources Sector ETF. Diversified resources exposure in a single trade

ASX: WDS (Woodside Energy) — Direct LNG exposure; a key beneficiary of elevated energy prices and Asian demand

ASX: BHP — Diversified miner with copper exposure, which benefits from both the energy transition and AI infrastructure build-out

ASX: NDQ — BetaShares NASDAQ 100 ETF. For investors wanting exposure to the US tech rally driving global equity highs

ASX: GMTL — Global X Rare Earth and Critical Metals ETF. Provides diversified exposure to a global basket of companies involved in the mining, refining and production of rare earth elements and other critical minerals used in clean energy and advanced technology applications.

The Bottom Line

Today's inflation data is a holding pattern, not a turning point. The RBA is watching to see whether three hikes have done enough — or whether persistent global energy pressures require one more move. Neither outcome is certain.

For investors, that uncertainty creates opportunity. Elevated fixed income yields are real and lockable today. Equities remain supported by earnings, but in an increasingly expensive market, diversification matters more than it did. Energy, resources, and financials continue to offer structural support for Australia's macro environment.

Market Wrap

Equities hit record territory. The S&P 500 closed at an all-time high of 7,519.12, with the Nasdaq and Asian tech-heavy markets in Taiwan and South Korea all reaching record highs, reinforcing confidence in the AI and semiconductor investment cycle.

Bond yields spiked then steadied. US 10-year Treasury yields briefly touched 4.6% and 30-year yields crossed 5% for the first time since the GFC, as markets repriced US rate expectations sharply higher. Yields have since pulled back slightly but remain at elevated levels that are increasingly competitive with equities.

Australian inflation eased — but not enough. The April CPI reading of 4.2% (down from 4.6%) was a step in the right direction, but with the trimmed mean still at 3.4% and unemployment only nudging higher, the RBA has no clear reason to move. The cash rate stays at 4.35% for now, and the next meeting is unlikely to bring a change.

The Iran War continues to set the floor under energy prices. Ongoing Middle East disruption kept oil and LNG prices supported through the week, underpinning Australian energy and resources stocks. Any diplomatic breakthrough remains the biggest potential market-moving event not yet priced in.

What We're Keeping an Eye on

Australia Q1 GDP data — June 3: Will confirm whether the economy is holding up under the weight of three rate hikes

US Jobs data — June 5: US labour market strength influences the Federal Reserve's path, which in turn shapes global rate expectations and the AUD/USD dynamic

Middle East developments — Any ceasefire or diplomatic progress on the Iran conflict would be a significant downside catalyst for energy prices and the inflation outlook

Important disclaimer: SelfWealth Pty Ltd ABN 52 154 324 428 (“Selfwealth”) (AFSL 421789). The information contained on this website is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser and/or accountant. Taxation, legal and other matters referred to on this website are of a general nature only and should not be relied upon in place of appropriate professional advice. You should obtain the relevant Product Disclosure Statement for any product mentioned and consider its contents before making any decision.

Most Recent Articles