Selfwealth

Key takeaways:

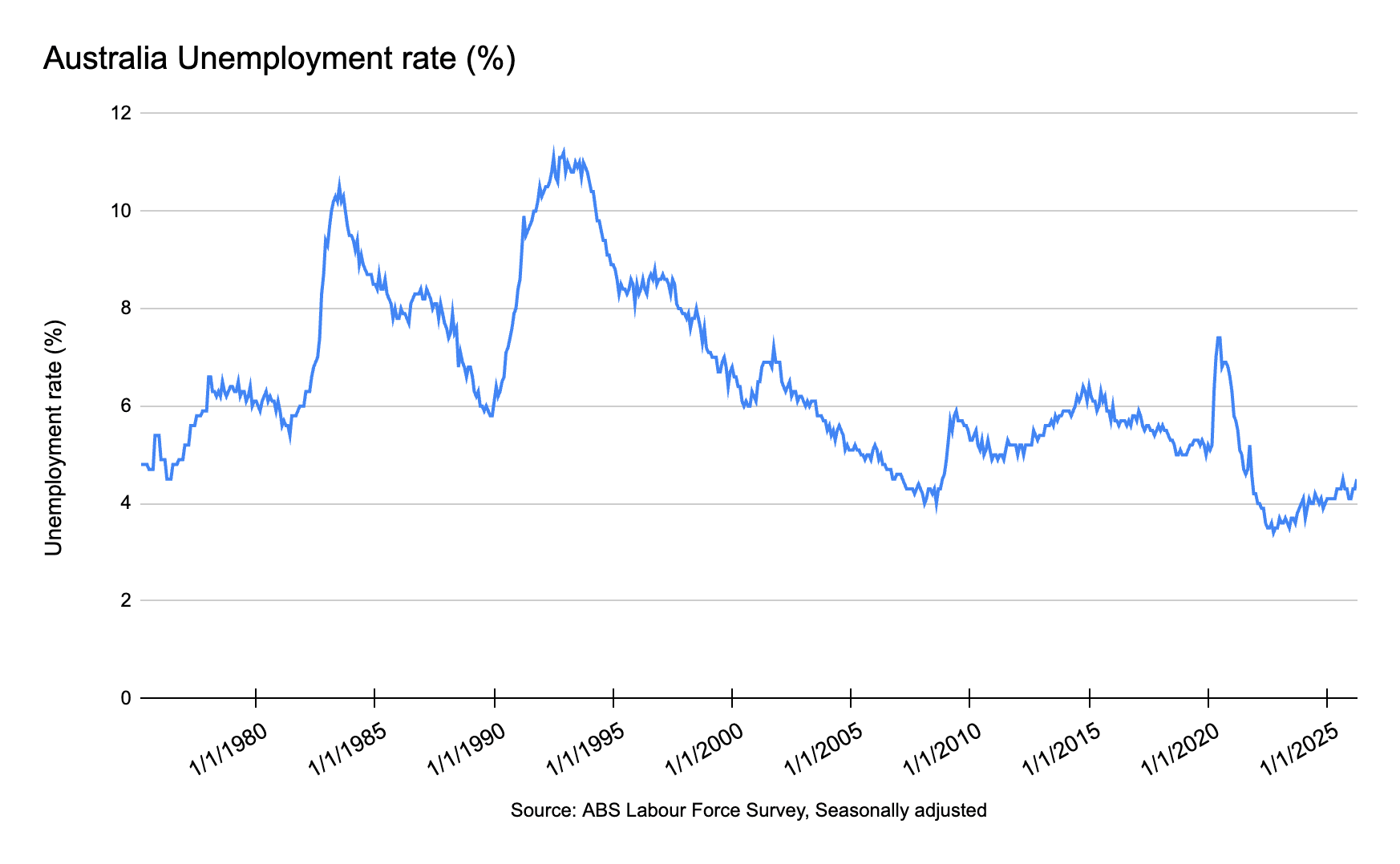

Unemployment ticked up to 4.5% in April — the labour market is still solid, but AI's shadow is growing

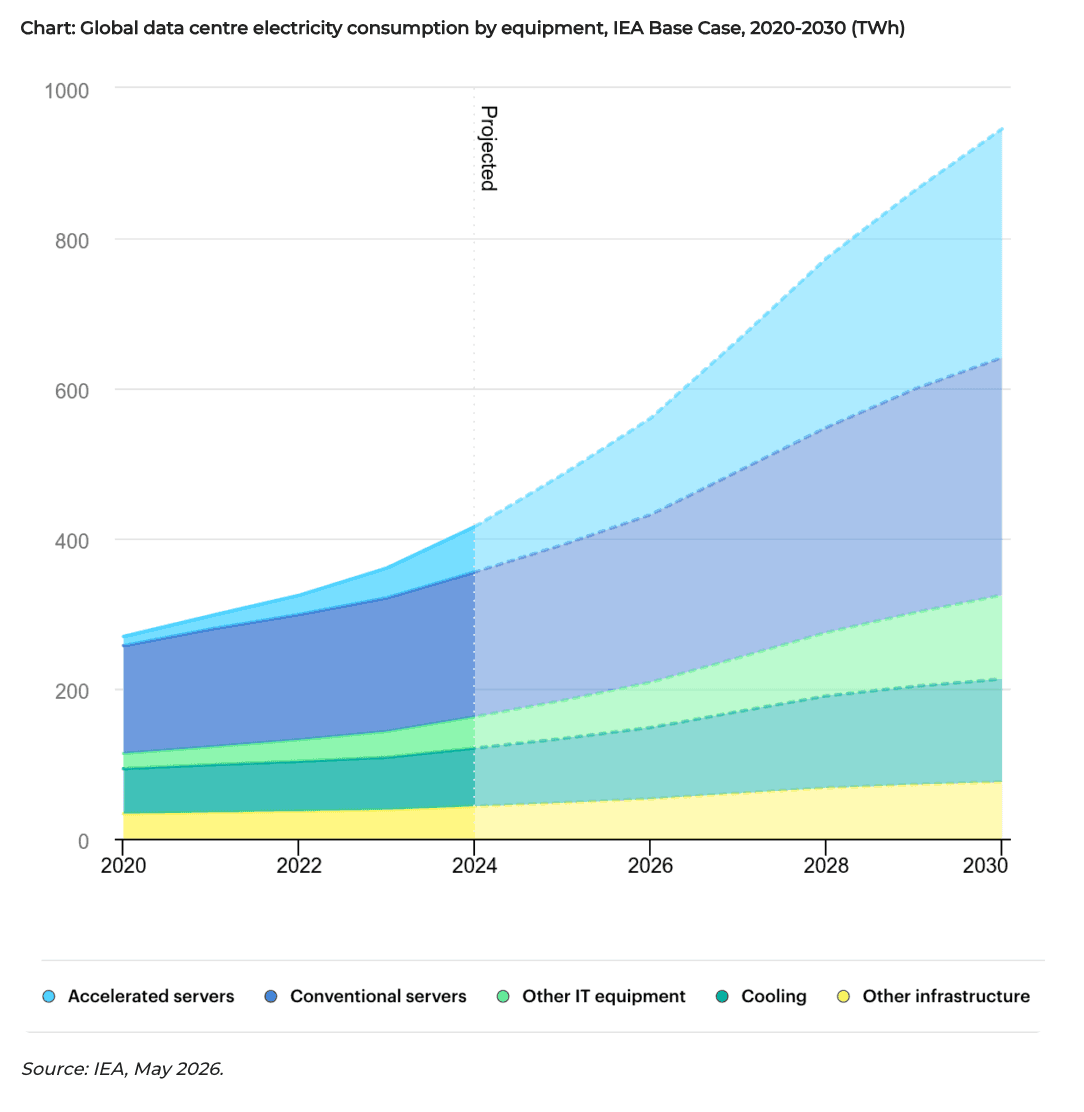

AI's energy demands are enormous and accelerating — data centre electricity use is set to more than double by 2030

The Iran conflict has turned energy security from a policy debate into an economic priority for governments worldwide

Australia's LNG position and critical minerals make it structurally well-placed — and the budget's decision to hold off on a gas tax was a positive for energy investors

ASX Materials and Energy have led the market in 2026; the drivers look to remain, but stretched valuations and a Middle East resolution are the key risks to the trade

Australia's Jobs Market: Steady, but AI is in the headlines

Australia's unemployment rate rose to 4.5% in April, up from 4.3% in March, according to data released today by the Australian Bureau of Statistics. On the surface, this remains reassuring — the labour market is relatively tight, with over 14.7 million Australians in work and participation rates close to record highs. That said, the uptick is worth monitoring in coming months to gauge whether the labour market is beginning to soften. For the RBA, today's print is unlikely to move the needle. The central bank reiterated at its latest meeting that it remains data-dependent, particularly on inflation, before making any further rate moves. A modest rise in unemployment alone does not compel it to act in the near term — if anything, an upward tick here may give the Board more reason to hold as it continues to assess the lagged impact of higher rates on the broader economy.

While the headline unemployment rate is steady, there are some subtle shifts beneath the surface. The latest industry breakdown of employment figures (February data) shows the Business Services sector has been relatively stagnant. This aligns with a broader trend playing out across recent earnings seasons, where a number of large companies have announced headcount reductions — citing AI either explicitly or implicitly. In Australia, WiseTech, Telstra, and Atlassian have all made cuts, and this week Standard Chartered announced a restructure targeting more than 15% of its corporate functions, attributed to AI. Overall, though, the Australian employment picture remains robust, with growth continuing in healthcare, education, construction, and mining.

Demand for AI is not slowing — and someone has to power it

It’s hard to go a day without hearing about AI, and its appetite for physical infrastructure is growing as fast as its profile. The International Energy Agency projects that global data centre electricity demand will more than double to around 945 terawatt-hours by 2030 — roughly equivalent to Japan's entire electricity consumption today. Big Tech has responded by contracting over 10 gigawatts of new nuclear capacity in the past year alone.

Goldman Sachs estimates US power demand will grow around 3.2% annually through 2030, with potential to reach 3.8% if "agentic" AI — the next generation of tools that run multiple models simultaneously in constant feedback loops — takes off faster than expected. Agentic AI is estimated to be 15 to 50 times more energy-intensive than today's chatbots.

Weathering the Storm

This sheer increase in AI demand for energy and physical infrastructure comes at a time when the Iran conflict has made energy security even more urgent. The disruptions in the Strait of Hormuz — through which around a quarter of the world's oil and liquefied natural gas (LNG) normally flows — have created one of the largest oil supply disruptions in history. Even if the conflict resolves, there will likely be downstream price shocks still to pass through, from fertilisers to chemicals to food.

Governments around the world have been jolted into action on energy independence in a way that years of policy debate could not achieve. When energy flows become less reliable, countries exporting more energy than they import are more secure. The United States suffered badly from the oil shock in the 1970s when it was dependent on Middle Eastern oil. Today, it is a net energy exporter – a status that kept its financial markets and economy much more resilient during the Iran conflict sell-off in March 2026.

Oil is not the only measure, though. China, though a net energy importer, has drawn on strategic reserves and a mature renewables ecosystem to buffer the impact. By contrast, an emerging economy like the Philippines – a net energy importer with little to fall back on – has proved to be much more vulnerable.

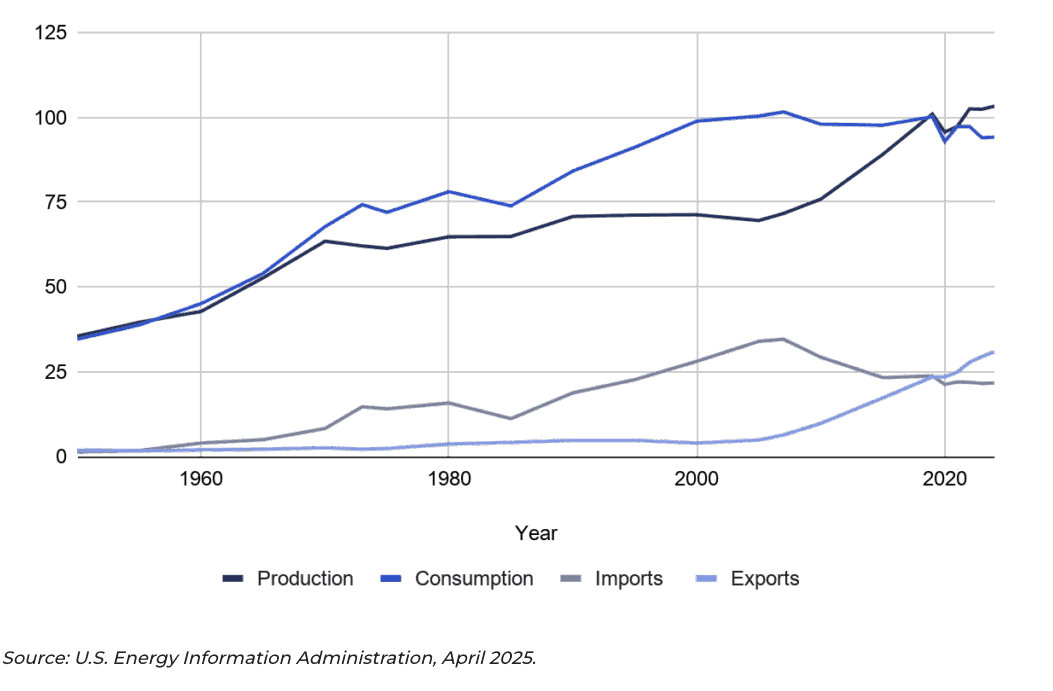

Australia finds itself in an interesting position here. It is a net energy exporter overall, thanks largely to its LNG production capacity. But it remains a net oil importer, which is why the federal government's recent budget contained a substantial $14.8 billion fuel resilience package designed to shore up domestic supply of fuel. Read our Budget analysis from last week.

Equally notable was what the budget did not include: a new gas tax. The government confirmed it will not introduce new levies on gas exports, stating that recent reforms to the Petroleum Resource Rent Tax (PRRT) are already delivering an adequate return to the Australian community. That decision is a positive for LNG producers — the sector avoids any added regulatory headwinds, leaving a cleaner outlook for investors.

The world has entered a new era where energy security can no longer be taken for granted, as demonstrated by the ongoing military conflicts in Iran and Ukraine. This will likely remain a key priority for governments in upcoming years as daily economic activity and increasing use of AI continue to underpin demand.

What This Means for Australian Investors

If you hold a diversified portfolio, you are likely already exposed to the parts of the economy that AI is reshaping: the software companies, the banks digitising their operations, the consumer businesses driving efficiency through automation.

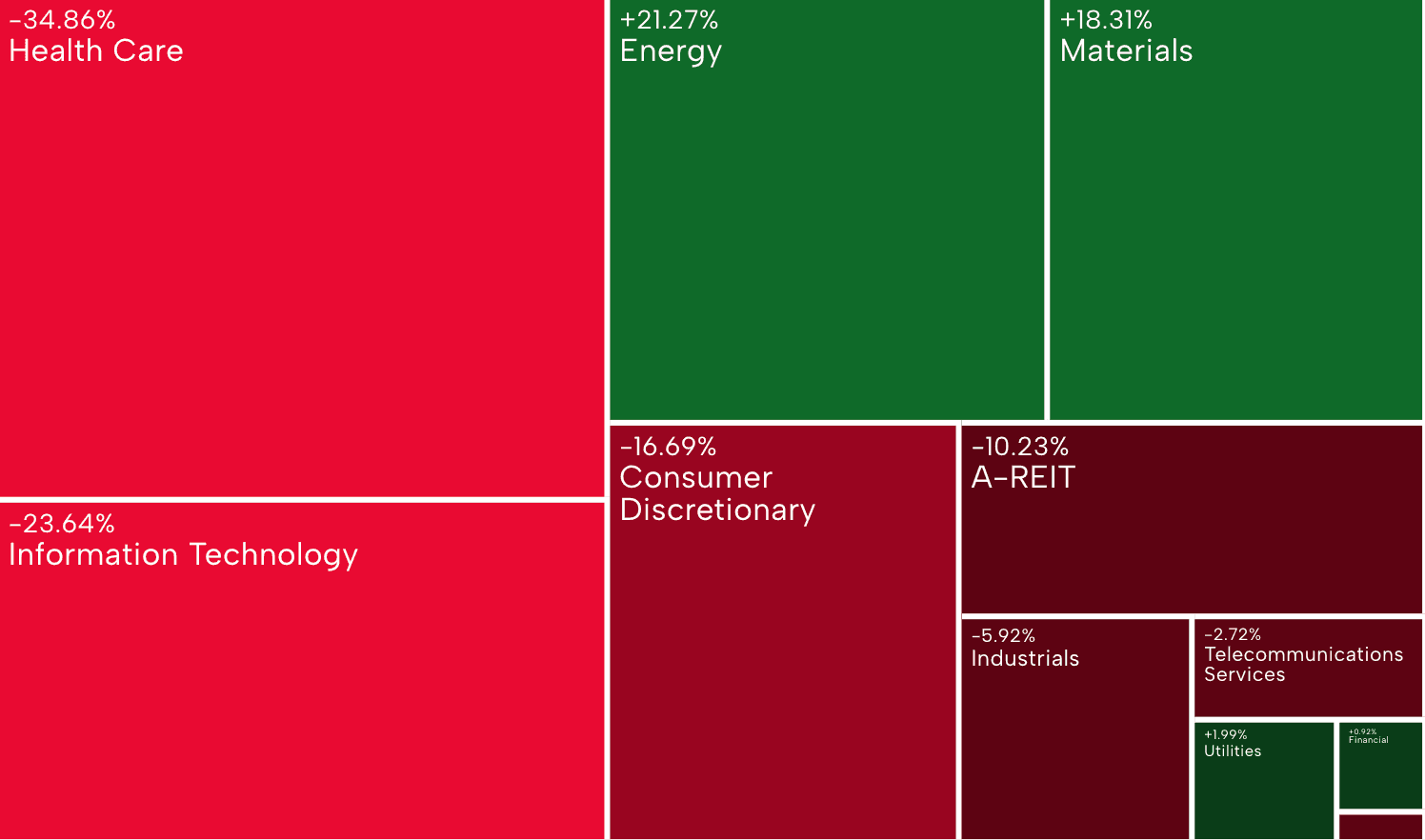

Energy and Materials take you one step further — into the fuel, metals, and infrastructure that all of those businesses depend on to operate. From that perspective, they can complement rather than duplicate what you already own. Benefiting from some of the tailwinds we discussed, the ASX Materials and Energy sectors have been the standout performers in 2026 — and the drivers could be structural, not just cyclical.

ASX sector performance as of May 19 over the past 6 months:

Source: asx.com.au

The race is now on to reduce dependence on vulnerable supply chains and diversify energy sources. That means nuclear, LNG, critical minerals, and the infrastructure to move and store all of it.

Nuclear and uranium have become a central part of the answer to the energy security challenge — always-on, carbon-free, and scalable. Globally, sustainable fund managers have been relaxing long-standing nuclear exclusions as energy security overtakes climate change as the primary policy driver. Microsoft, Amazon, and Google have each signed landmark nuclear power deals. In Australia, the pathway remains politically contested, with nuclear safety and costs expected to feature in the next election.

Energy infrastructure — pipelines, LNG terminals, and power grids — is in surging demand as countries look to secure supply that does not flow through a chokepoint. Around 40% of Europe's power grids are more than 40 years old, and $600 billion annually is estimated to be needed to meet decarbonisation and electrification goals by 2030.

Critical minerals — cobalt, lithium, copper, rare earths — go into everything from batteries to magnets at the heart of clean energy production, transmission, and storage. China controls over 60% of rare earth mining and 90% of processing, creating a strategic imperative for the West to secure alternative supply. Australia sits at the centre of that alternative.

Two risks are worth watching: valuations have risen as these stocks have rallied, and energy prices remain tied to geopolitics. A resolution in the Middle East could remove a meaningful part of the commodity tailwind, even if the structural energy security theme endures.

For investors seeking exposure to these themes, exposure to rare earths and critical minerals can take several forms, each with different risk characteristics and sensitivities. Some investors gain exposure through mining and processing companies, whose performance can be influenced by factors such as production costs, operational outcomes, regulatory settings and broader equity market conditions. For now, Australian investors seeking domestic nuclear exposure will need to look at uranium producers rather than power generators. Others use exchange-traded funds (ETFs), which may provide diversified exposure to rare earth and critical mineral-related assets. Examples include individual companies and funds such as:

Lynas Rare Earths (ASX: LYC)

One of the world's largest producers of rare earth materials outside of China, with mining operations in Australia and processing facilities across Australia and Malaysia.Pilbara Minerals (ASX: PLS)

A leading Australian lithium producer focused on the Pilgangoora lithium-tantalum project in Western Australia, providing exposure to battery-grade critical minerals.Global X Rare Earth and Critical Metals ETF (ASX: GMTL)

Provides diversified exposure to a global basket of companies involved in the mining, refining and production of rare earth elements and other critical minerals used in clean energy and advanced technology applications.

Paladin Energy (ASX: PDN)

An Australian uranium producer with operations primarily at the Langer Heinrich Mine in Namibia, providing direct exposure to uranium production and price movements.VanEck Uranium and Energy Innovation ETF (ASX: URAN)

Provides exposure to a global basket of companies involved in uranium mining, nuclear energy generation and related energy innovation technologies.

Market wrap/In review

The Budget has been released — now all eyes turn to what the Government can legislate of their proposed changes

Attention now shifts from what was announced to what can actually pass parliament, with a number of measures requiring legislative approval

Australia's unemployment rate ticks up to 4.5%

Australia's labour market remains relatively tight, however, the unemployment rate increased in April to 4.5% from 4.3% in March. The result offers the RBA little reason to move rates in the near term, with the board still focused on inflation as its primary guide.

AI and energy usage remain firmly in the market spotlight

AI's appetite for power continues to reshape the global energy investment outlook, with data centre electricity demand on track to more than double by 2030. The Iran conflict has added urgency to the conversation, turning energy security from a long-term policy theme into an immediate economic priority for governments worldwide. For Australian investors, the combination of LNG exposure, critical minerals, and a budget that avoided new gas levies leaves the local energy and materials sectors well positioned relative to global peers.

ASX sector performance as of May 19 over the past 6 months:

Source: asx.com.au

What we’re keeping an eye on next week:

Australian Inflation data: May 27

Australia Q1 GDP data: June 3

US Unemployment data: June 5

Important disclaimer: SelfWealth Pty Ltd ABN 52 154 324 428 (“Selfwealth”) (AFSL 421789). The information contained on this website is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser and/or accountant. Taxation, legal and other matters referred to on this website are of a general nature only and should not be relied upon in place of appropriate professional advice. You should obtain the relevant Product Disclosure Statement for any product mentioned and consider its contents before making any decision.

Most Recent Articles