Key Takeaways

The government has scrapped the 50% Capital Gains Tax (CGT) discount for assets held longer than 12 months, replacing it with an inflation-indexation model — reverting to the system in place before 1999. This change applies to all asset classes, not just property.

A new 30% minimum tax on real capital gains has also been introduced, limiting the ability to time asset sales to low-income years.

For investors holding high-growth assets, the combination of indexation and the minimum tax could mean a higher tax bill over time, though the real impact will depend heavily on inflation and individual circumstances. Slower-growing, income-focused portfolios may be less affected.

There is a transition period to 1 July 2027, after which the new rules apply to gains accruing from that date. Short-term gains (assets held under 12 months) are unchanged throughout.

Tax settings matter at the margin, but your risk profile, return expectations and time horizon should still drive allocation decisions. Use the transition period to get advice before making any changes.

What's Changed

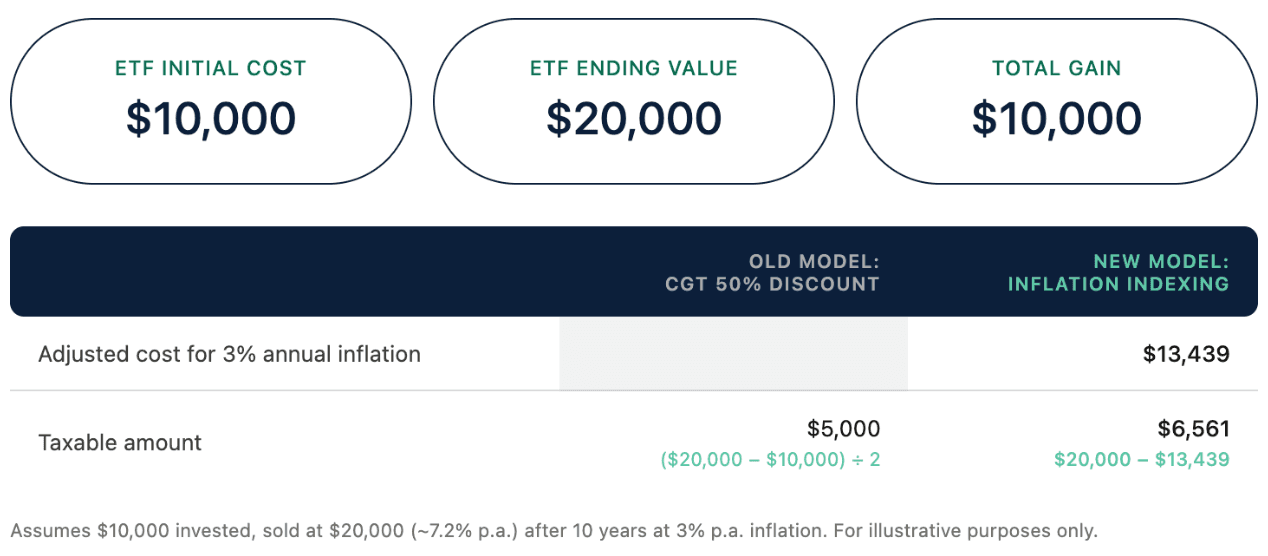

Australia's 50% capital gains tax discount — introduced in 1999 — has been significantly reformed in this week's Budget. In its place, the government has introduced a return to inflation-indexation, where your cost base is adjusted for CPI and you pay tax on 100% of any gain above that. The only relief is that purely inflationary growth goes untaxed.

This is a meaningful shift. To highlight the change, let’s assume an environment of 3% annual inflation. Under the old rules, if you bought an ETF for $10,000 and sold it a decade later for $20,000 (~7.2% annual return), you would effectively pay tax on a $5,000 gain. In the new rules, you would pay tax on $6,561.

Importantly, the government has built in a one-year transition window. For assets already held, the 50% discount applies to gains that accrued up to 1 July 2027. Gains accruing after that date fall under indexation and the minimum tax. To work out how much of your gain falls under each regime, you'll need to establish what your asset was actually worth on 1 July 2027 — that value becomes the dividing line. Gains up to that value get the 50% discount; gains above it from that date onward are subject to indexation and the minimum tax.

Alongside indexation, the government has introduced a 30% minimum tax on real capital gains from 1 July 2027 for most investors outside of the superannuation and pension system. Previously, one of the key advantages of holding growth assets was the ability to time a sale to a year when your marginal rate was low — typically retirement. The minimum tax floors your rate at 30% on real gains regardless of other income that year, substantially reducing that strategy.

It's worth noting these changes have been announced but still need to pass through parliament before becoming law. The final details may evolve as the legislation is drafted.

Does This Apply to Shares and ETFs?

Yes. While a lot of media speculation leading up to the Budget has focused on the property market, the reform applies to all asset classes — shares, ETFs, and investment property.

The CGT treatment of domestic and international equities remains the same under the new regime as it was under the old — indexation applies equally to both. The structural tax advantage of ASX equities over global holdings continues to sit largely within the franking credit system, which is unchanged.

What's Not Changed

Short-term capital gains - on assets held less than 12 months - are unaffected. Your full gain continues to be included in taxable income at your marginal rate.

The CGT changes do not apply to assets held inside superannuation. Super funds - including SMSFs - retain their existing CGT treatment

Carry-forward capital losses remain in place and are unaffected - losses are still measured on nominal cost basis, not inflation-adjusted cost, consistent with how the pre-1999 system worked.

How the Transition Works

The government has not proposed a revaluation of all existing holdings. Instead, for assets held before 1 July 2027 but sold after, the 50% discount applies to gains accrued up to that date, while indexation and the minimum tax apply to gains from that point forward. The asset's market value at 1 July 2027 becomes the new cost base for the post-commencement period.

Taxpayers can either seek a formal valuation or use an ATO-approved apportionment formula. The ATO is expected to provide tools to assist with this calculation.

For assets acquired after Budget night (12 May 2026), the same framework applies — the 50% discount covers any gain to 1 July 2027, with indexation applying thereafter.

In the property space, there is one notable carve-out: investors who purchase new residential builds retain the choice between the 50% discount or indexation when they eventually sell. This exemption does not apply to established dwellings or to shares.

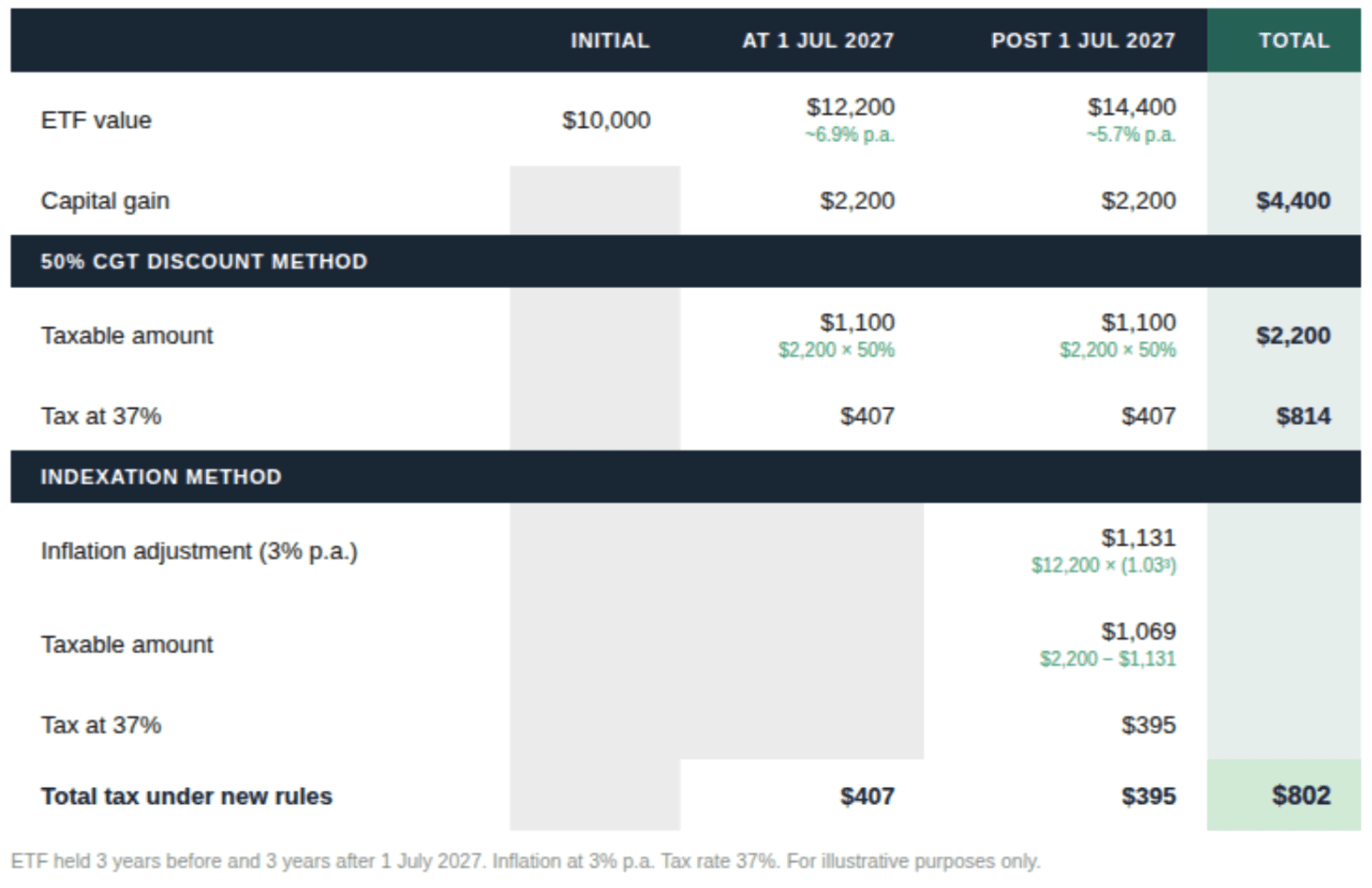

Below is a worked example. Say you bought an ETF for $10,000. You’ve held it for 3 years before 1 July 2027 (growing to $12,200), and held it for another 3 years after 1 July 2027 (growing to ($14,400). Your total gain is $4,400 across the two regimes, however you will have to apportion tax according the July 2027 date:

What It Means for the Market

Quality Income vs Growth stocks

At the margin, these changes could shift the relative appeal for investors towards more income (dividend paying) stocks. Under the new CGT policy, high-growth, long-held assets are most exposed in a modest or low inflation environment (such as that of the past decade). In the past, investors with stocks that have grown well above inflation for many years such as global tech stocks received some tax protection from the 50% discount. Now, indexation only shelters the inflation slice and now everything above it is fully taxable.

This means investors with a low cost base face a particular sting. If you buy shares at a few dollars that rise significantly, inflation-indexing your tiny original cost base gives little relief.

For investors already drawn to income-focused ASX stocks, these changes provide a modestly stronger tax rationale for that preference — particularly for high-quality stocks paying franked dividends, where the imputation system remains fully intact. This isn't a signal to restructure a portfolio, but it is a genuine shift in the relative after-tax calculus depending on your inflation outlook and desire for returns via income or a capital gain.

It’s worth noting, on the other hand, if your assets grow more slowly, then indexation could leave you with a smaller tax bill than the 50% discount would have. In a period of elevated inflation, then slower growth sectors or assets might have reduced tax on sale.

Property vs Equities

The changes to CGT have primarily been discussed in the lead up to the budget in reference to targeting the housing market, such as those findings in the 2026 Senate Committee on CGT. The Budget has limited the use of negative gearing allowances for investment properties, and accordingly equities may become more appealing relative to property for those seeking a return. For investors weighing up where to deploy capital, shares offer something established property doesn't — liquidity, flexibility, and after this Budget, comparatively less policy risk.

Inflation and the RBA

Capital gains tax reform on its own won't move the needle for the Reserve Bank. The Budget is designed to be revenue neutral, which if it holds, limits any new demand pressure. That said, markets will still scrutinise the broader spending measures — revenue neutrality is a Treasury forecast, not a guarantee, and the RBA will be watching the data rather than taking the Budget at its word.

How the Indexation Calculation Actually Works

Under the new system, your inflation-adjusted cost base is calculated using the ATO's official quarterly CPI figures. The formula is:

Indexation factor = CPI at sale quarter ÷ CPI at purchase quarter

You then multiply your original cost base by that factor to get the inflation-adjusted cost base, and pay tax on the gain above that — subject to the 30% minimum tax rate floor. The RBA publishes an approximate inflation calculator on their site which can be a useful gauge.

Example: You bought shares for $10,000 in the March 2020 quarter (CPI: 114.1). You sell in the June 2030 quarter (hypothetical CPI: 145.0). Your indexation factor is 145.0 ÷ 114.1 = 1.271. Your adjusted cost base becomes $12,710. If you sell for $25,000, your taxable gain is $25,000 − $12,710 = $12,290 — rather than the full nominal gain of $15,000.

For many share investors, there is typically one purchase cost plus brokerage, so the calculation is relatively contained. Where it gets more complex is for investors with: multiple parcels acquired at different times (each indexed separately from its own purchase quarter); dividend reinvestment plan shares accumulated over many years at many different cost bases; or property, where stamp duty, legal fees, and capital improvements are each indexed from the quarter they were incurred.

This administrative complexity was actually one of the stated reasons the government replaced indexation with the 50% discount in 1999, and why many other countries have maintained a flat rate model. Whether the government introduces any simplification measures — such as a single blended index rate per asset — will become clearer as the Budget legislation is released.

What This Means for Asset Allocation

The change to tax policy is one factor in a portfolio but not necessarily a reason to restructure. Tax settings matter at the margin, but asset allocation decisions are driven far more by risk profile, return expectations, liquidity and time horizon. That said, a few things are worth noting:

Franked dividends become comparatively more attractive at the margin — not because anything has changed in the imputation system, but because the CGT treatment of long-term growth assets has become less generous, narrowing the gap. This isn't a signal to rotate out of growth into income — investors have always held both for good reasons — but it reinforces why Australia's imputation system remains a genuine structural advantage for high quality domestic equities that pay franked dividends.

Global diversification is still primarily a risk and return question, not a tax one. Australian investors have historically been biased toward ASX-listed equities, with franking credits being a real and rational reason. The CGT treatment of international equities hasn't changed — indexation applies equally whether you hold domestic or global assets. The case for diversifying was always about reducing concentration risk and accessing sectors underrepresented on the ASX, and that case stands independently of this Budget.

You have time — use it well. The one-year transition period to 1 July 2027 is a genuine window to model your position, speak with your financial advisor and accountant, and make considered decisions. Nothing needs to happen urgently.

The Bottom Line

The CGT changes confirmed this week represent the most significant shift to investment taxation in Australia since 1999. For long-term share and ETF investors — particularly those holding high-growth assets — the new regime could generally mean more tax over time in a lower inflationary environment. The transition period to 1 July 2027 provides some breathing room to understand your position. The key message for most investors is to hold your course, use the time available to get advice, and avoid making structural changes to your portfolio before you've modelled what the new rules actually mean for your specific situation.

Our Director of Investment Strategy, Rob Wilson, was recently featured in leading financial publications including Bloomberg and the Australian Financial Review, sharing expert analysis on the Federal Budget and what it means for Australian investors.

Read more of Rob’s commentary:

Important disclaimer: SelfWealth Pty Ltd ABN 52 154 324 428 (“Selfwealth”) (AFSL 421789). The information contained on this website is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser and/or accountant. Taxation, legal and other matters referred to on this website are of a general nature only and should not be relied upon in place of appropriate professional advice. You should obtain the relevant Product Disclosure Statement for any product mentioned and consider its contents before making any decision.

Most Recent Articles