Key Takeaways

RBA has hiked (again) to bring the cash rate to 4.10%. We think it can rise further still.

Price rises have been sticky, with the economy firing on all cylinders. The oil shock from the Iran war can further complicate the fight against inflation.

Now might be a good time to review your personal finances and investment portfolio:

Mortgage holders may wish to review their refinancing options or build up their offset account. Expect mortgage rates to stay higher for longer.

Stay invested. That’s historically the best strategy for most investors. Find out how Selfwealth’s new “auto invest” function can help you do this.

Stay disciplined, stay diversified. Don’t put all your eggs in one basket. Be selective about what you choose in Australia (some segments are more impacted by rate hikes than others).

Read to the end to find out how you can put these insights into action!

What Happened

The Reserve Bank of Australia (RBA) raised its cash rate 25 basis points to 4.10% on Tuesday. This followed the February hike, which made Australia’s central bank the first major monetary authority to raise rates in 2026. It also marked the first consecutive RBA hikes in almost three years.

Policymakers pointed to inflation stemming from “capacity” challenges as the primary reason for their decision. This means the economy as a whole is running above its “speed limit” i.e. growing faster than the available workforce, physical infrastructure, and supply chains can accommodate.

The RBA is vigilant and bracing for any knock-on effect of the war in Iran. “Short-term measures of inflation expectations have already risen,” said the RBA’s statement.

What It Means

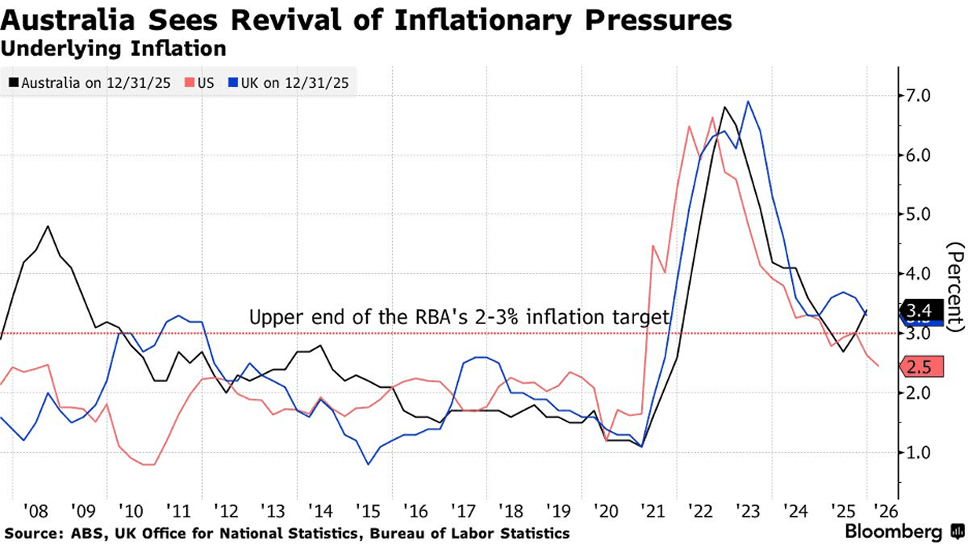

By hiking this week, the RBA is trying to get ahead of the curve. Inflation is at 3.4% and heading towards the 4% handle. We expect at least one other hike this year, potentially in the next meeting in May.

On balance, policymakers are more worried about runaway prices than a growth slowdown or consumption crunch. "It will be much worse if inflation gets built into the fibres and then we will see the costs of everything going up, and that will be a much worse outcome," Governor Michele Bullock said after the decision was announced on Tuesday.

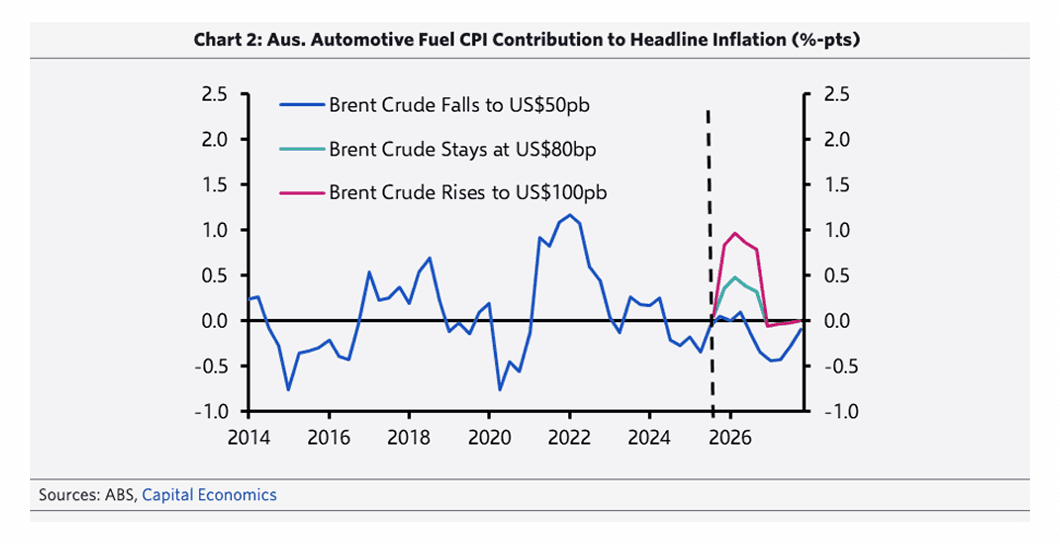

The Iran conflict loomed large. The following chart projects the price impact on Australia from global oil prices. And this is before accounting for the cost that businesses, which also consume fuel, would have to pass through to consumers. Researchers at Capital Economics believe the Consumer Price Index (CPI) will cross 4% this year in all three scenarios.

Why It Matters

It was a close call. Four out of nine members of the board voted against a hike. According to the governor, they agreed on the need to hike but worry that the central bank is moving too early.

This is because the outcome of the war in Iran remains uncertain, and inflation pressure from the war could be lower than markets fear. What was designed to be a pre-emptive hike could turn out to be a hand-brake on growth, pressuring the economy more than the RBA intends to.

Unlike the US or the UK, mortgages in Australia last years rather than decades. Hence a hike in the “cash” rate (i.e. the short-term rate) is more keenly felt by households here than in other countries. Over 75% of consumers expect mortgage rates to increase over the next 12 months as of March, according to the Westpac-Melbourne Institute Mortgage Rate Expectations Index.

Markets will now watch closely for clues on how the economy is doing. The February employment report this week will be one such datapoint, followed by inflation data next week.

What Does This Mean for My Money?

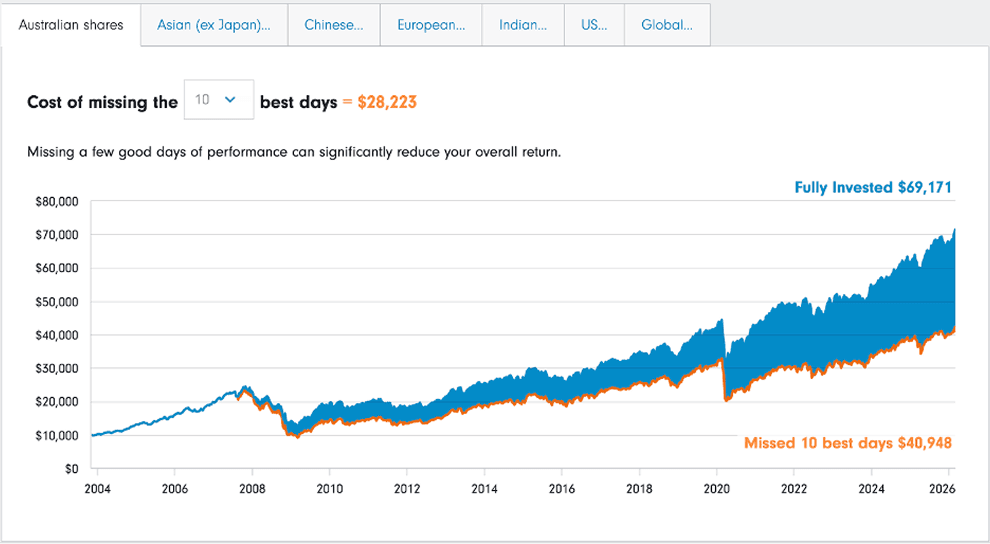

Research has shown that “time in the market” beats “timing the market”. The chart below from Fidelity shows the gains an investor would have given up on by missing the 10 best days in ASX since 2004. This is why we recently launched “auto invest” – to help you stay invested and build long-term wealth. Discover more about the new function here.

Source: Datastream, Fidelity International, as of March 2026.

Note: This chart shows how a notional $10,000 investment would have been affected if the 10 best days were missed. Daily returns of the ASX/S&P 200 Accumulation index (Source: Datastream), from 31 Oct 2003 to 04 Mar 2026.

Investment

There are adjustments you can make to your portfolio. With higher rates and greater uncertainty, it would not be a bad idea to maintain cash levels. A high-interest cash ETF could provide income with flexibility, allowing you to seize opportunities when they emerge.

In equities, be selective. Financials benefit from wider margins, but loan growth could be hurt if the economy splutters. Miners and energy names are more insulated from the domestic rate cycle, and could benefit from the elevation in oil prices. By contrast, sectors like consumer discretionary are much more exposed to lower consumer spending and confidence.

Hikes are generally bad for bonds, but not all bonds are created equal. 10-year Aussie bonds are now offering close to 5% yield. These bonds tend to gain in value once the economy cools due to the RBA’s rapid tightening. This means right now could be a sweet spot to lock in income and position for capital gains.

Across asset classes and geographies, diversification remains essential. As we pointed out before in this guide, there are plenty of long-term opportunities for investors willing to look beyond the home market for growth.

Finally, a word on FX. The Aussie dollar has been one of the strongest currencies globally this year, in part because of expectations of RBA hikes. But much of that strength is in the price, and investors rushing for the safety of the USD is taking some shine off the AUD. Analysts at ING believe it will be harder for AUD to continue making standout gains, at least in the near future.

Here’s a list of ETFs available on Selfwealth that can help you diversify and build resilience in your portfolio.

Cash

AAA (BetaShares Australian High Interest Cash ETF) invests in bank deposits and pays the cash rate.

ISEC (iShares Enhanced Cash ETF), a slightly higher risk-reward alternative, holds short-term money market instruments and floating-rate notes.

Equities

VGS (Vanguard MSCI Index International Shares ETF) holds over 1,000 large-cap companies in the US and across the rest of the developed world, providing global diversification.

OZF (SPDR S&P/ASX 200 Financials EX A-REIT Fund) tracks Australia's largest banks and insurers.

OZR (SPDR S&P/ASX 200 Resources Fund) builds broad exposure to Australia's local mining and energy heavyweights.

FUEL (BetaShares Global Energy Companies ETF) invests in the world's largest energy giants, available on a currency-hedged basis, protecting you from FX fluctuations.

Fixed Income

VBND (Vanguard Global Aggregate Bond Index ETF - Hedged) invests in thousands of high-quality, fixed-income securities from governments and corporations around the world, providing defensive diversification.

AGVT (BetaShares Australian Government Bond ETF) focuses specifically on longer-dated Australian government bonds.

Commodities

GOLD (Global X Physical Gold Structured): Backed by physical gold bullion held in London vaults, tracks the spot price of gold.

BCOM (Global X Bloomberg Commodity Complex ETF): Provides broad, unhedged exposure to a massive basket of global commodities via futures contracts, including energy, agriculture, precious metals, and industrial metals.

Personal Finance

Mortgage holders will feel the squeeze first. With a high proportion of variable-rate and short-term fixed mortgages, repayments are likely to rise further in the coming months. Even another modest 25 basis points increase can add hundreds of dollars annually to repayments on an average loan. For borrowers, this is a good time to review refinancing options, consider fixing a portion of the loan (if suitable), or building a buffer in an offset account.

Housing dynamics may soften at the margin. Higher borrowing costs reduce purchasing power, which can weigh on property prices and slow down demand. For prospective buyers, this could mean less frenzied competition, but not necessarily significantly cheaper homes because of Australia’s existing structural housing shortage and population growth.

Debt management becomes more critical. Beyond mortgages, interest on credit cards and personal loans is also likely to rise. Prioritising high-interest debt repayment delivers a risk-free return equivalent to the interest saved, which is often far higher than what’s available in markets.

Inflation remains the silent drag. Even if headline inflation stabilises, essential costs – energy, insurance, and food – may stay elevated, particularly if global oil prices rise further. This reinforces the need for budgeting discipline and maintaining an emergency fund that reflects higher living costs.

Important disclaimer: SelfWealth Pty Ltd ABN 52 154 324 428 (“Selfwealth”) (AFSL 421789). The information contained on this website is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser and/or accountant. Taxation, legal and other matters referred to on this website are of a general nature only and should not be relied upon in place of appropriate professional advice. You should obtain the relevant Product Disclosure Statement for any product mentioned and consider its contents before making any decision.

Most Recent Articles