Key Takeaways

Inflation can be driven by supply or demand factors. Too much or too little are both bad for the economy.

Central banks typically hike interest rates to tame inflation – that’s what the RBA is doing right now.

Markets expect the current oil supply shock to be temporary, with corresponding slowing demand eventually bringing prices – and interest rates – down.

Market dislocations is an opportunity for disciplined investors: higher income, undervalued assets. Keep dollar cost averaging.

Back to Basics: What is inflation?

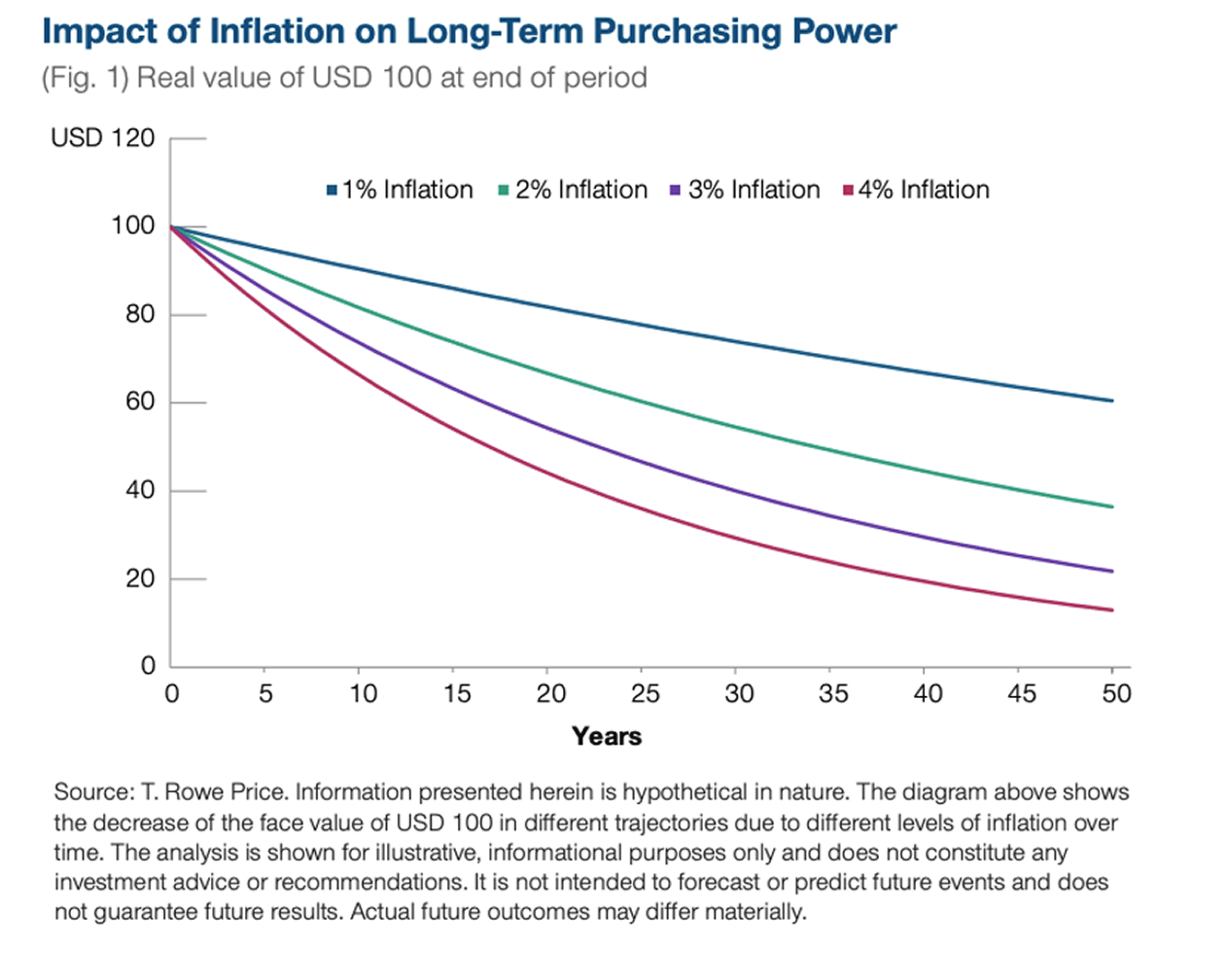

Inflation describes the rise in prices across an economy. Its most obvious impact is the erosion of purchasing power: $100 today buys less than $100 a decade ago. A few factors could lead to inflation:

Demand: Economy booms, consumers spend more, leading to price rises. This could happen when unemployment is very low and consumer confidence is high.

Supply: A surge in “input” costs (e.g. oil, wages, freight prices) forces businesses to raise prices. Examples: 1970s oil supply shock, 2022 war in Ukraine.

Currency weakness: Imports become more expensive as one’s currency weakens.

Self-fulfilling prophecy (“wage-price spiral”): Workers worried about rising prices demand higher wages (in absence of evident inflation). Cost passed on to consumers.

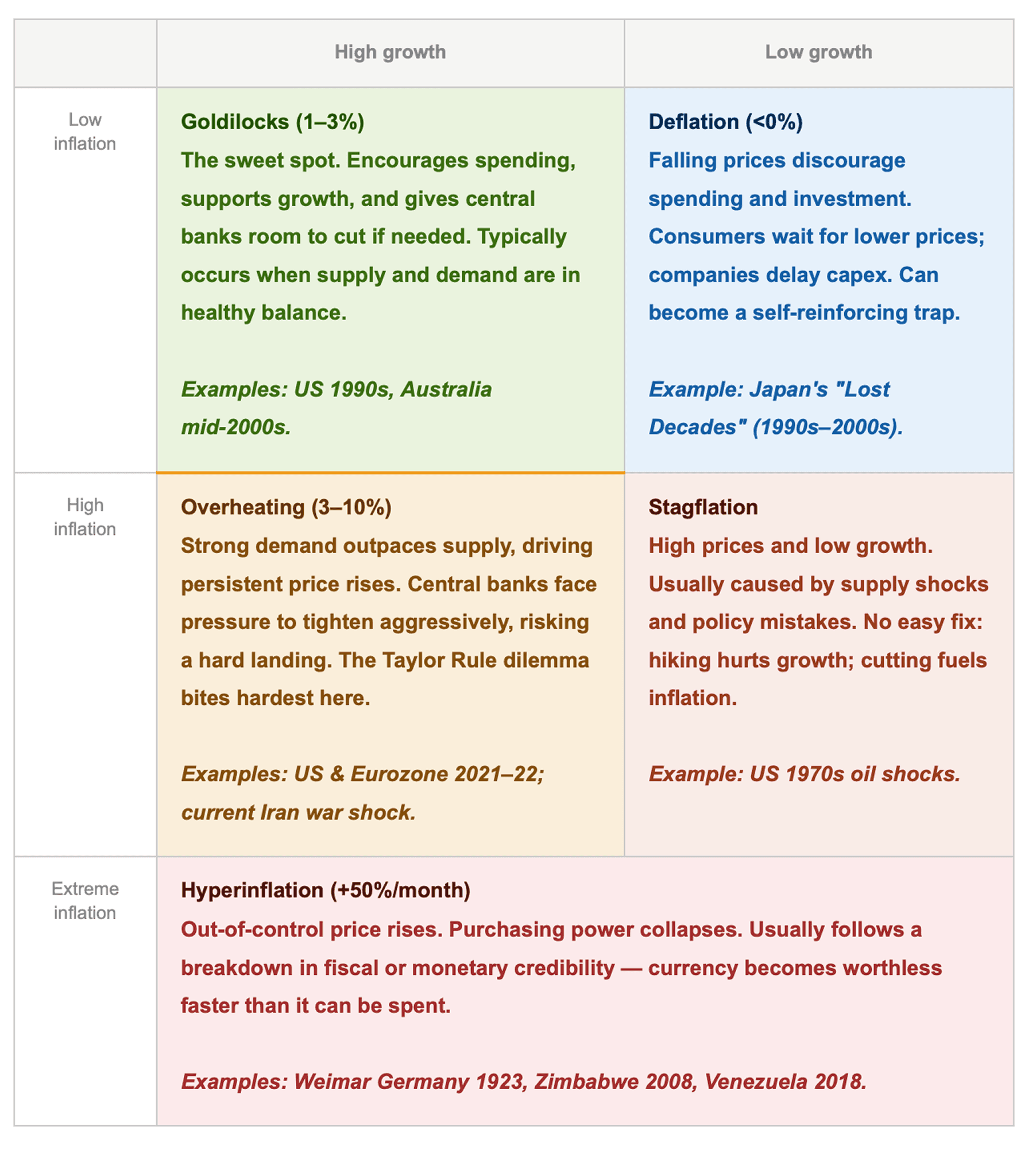

A bit of inflation is good for growth, spurring consumers to spend now rather than later and lifting corporate profits. Having none at all gives you the opposite.

Most developed economies aim for roughly 2% inflation. For a developed economy, Beyond 3%, every 1 percentage point of inflation rise in a developed economy typically reduces about 0.1-0.2% off “real” GDP growth (i.e. growth after taking account of inflation), according to research by the International Monetary Fund.

2. How do countries deal with inflation?

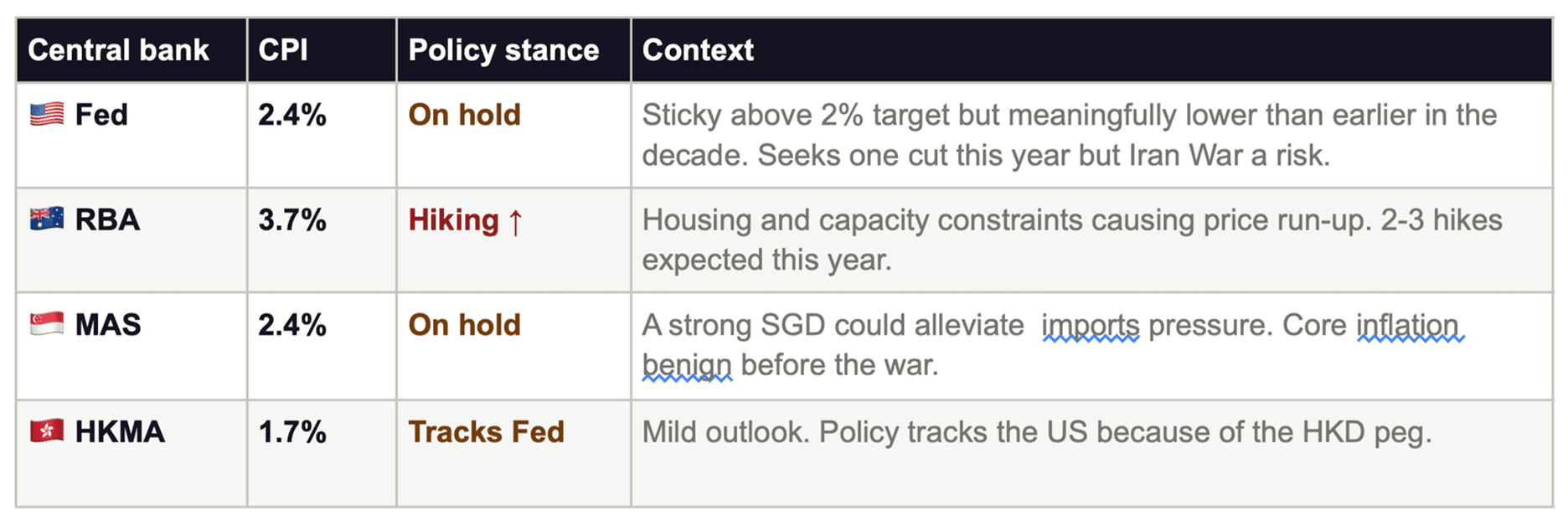

Inflation is primarily managed through monetary policy. Most central banks, like the US Federal Reserve, use interest rates as their main lever. Higher rates cool demand by making borrowing expensive, while lower rates encourage credit to flow (when they overdo this and allow too much money in the system, however, central banks can cause inflation). In Australia, the benchmark rate is the cash rate which is controlled by the Reserve Bank of Australia (RBA).

History offers two paths to ending inflation:

The hard way: Central banks engineer a hard landing. The Fed’s brutal 1980–82 rate hikes in the US crushed inflation from ~14% to ~3%. But they also caused a severe recession and unemployment north of 10%

The “easy” way: Let supply catch up with demand. The 1990s showed that a soft landing is possible but rare. The key variable is inflation expectations: once they become "unanchored" (as in the 1970s), a second wave is almost inevitable.

A useful rule of thumb here is the “Taylor Rule”: to genuinely tighten financial conditions and cool the economy, central banks need to raise rates by roughly 1.5 percentage points for every 1 percentage point in excess of the pace of inflation. Raising rates by less simply means policy is still accommodative, just a little less so.

What’s the inflation outlook right now?

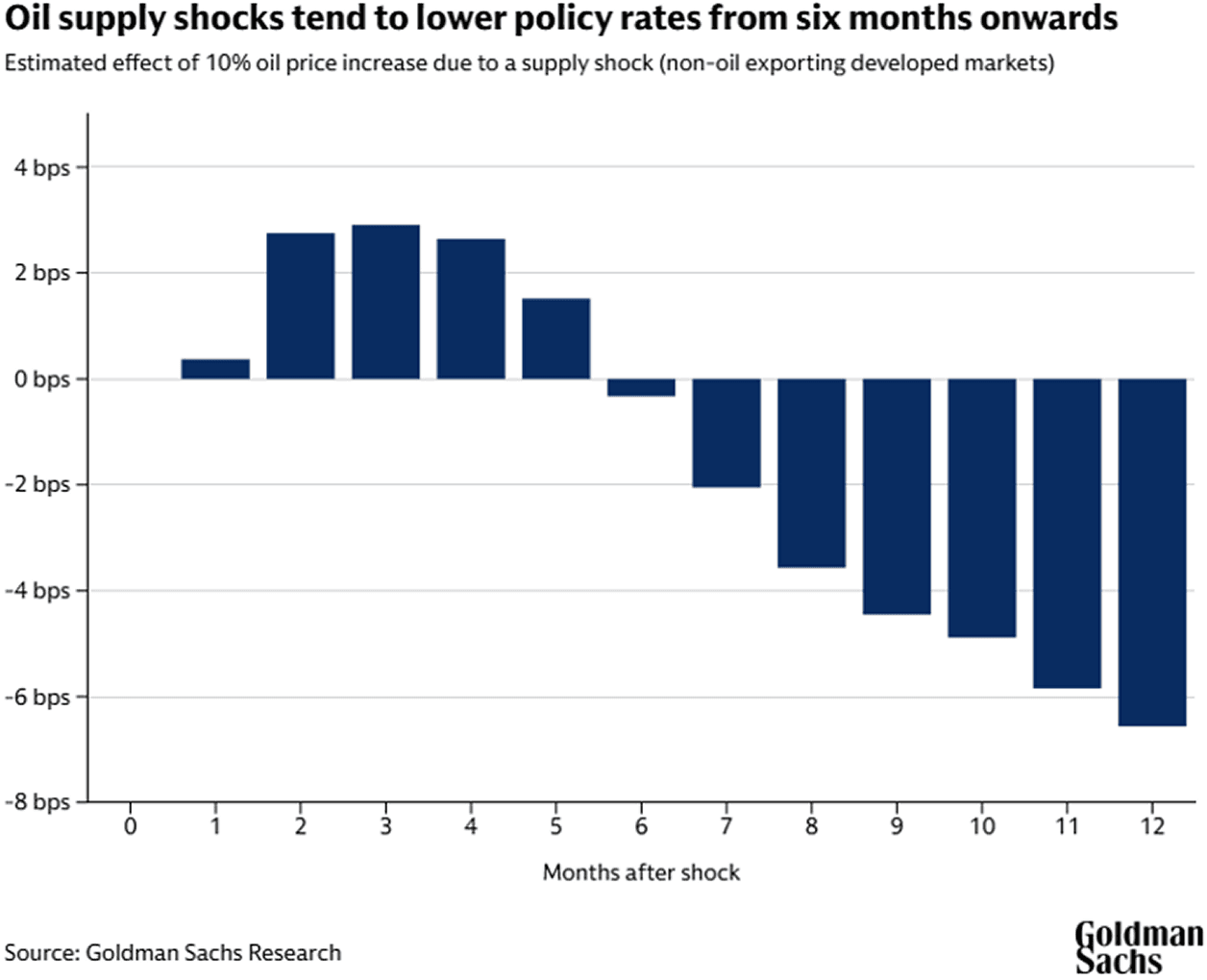

Markets have priced in rate hikes across most G7 economies since the outbreak of the Iran war. But history suggests this may be premature: supply-driven oil shocks tend to lift rates only briefly before growth concerns take over, pulling rates back down within six to twelve months.

This is because supply shocks simultaneously dampen growth and push up unemployment. Over time, those headwinds tend to outweigh the inflationary impulse, shifting central banks' priority from fighting inflation to supporting the economy. Central banks may find themselves unwinding hikes sooner than expected.

Oil futures are in “backwardation” at the time of writing, meaning it’s more expensive to buy oil in the near future than in the longer run. That indicates markets expect the current disruption to be temporary.

While it is true that the ultra-low inflation of the 2010s isn’t coming back (2% looks more like a floor than a ceiling), meaningful disinflationary forces remain. AI productivity gains are beginning to materialise, US rents are falling as record housing supply hits the market, wage growth has softened for most workers, and Chinese exporters redirecting cheap goods from the US (because of tariffs) are also bringing downward price pressures in the rest of the world.

What does this mean for my money?

Inflation feels unsettling right now because the usual defences aren’t working, with the “safety” of bonds and gold seemingly fading. But the lesson from history is reassuring: supply shocks eventually resolve, either because demand cools and rates fall, or because supply constraints ease and prices normalise. Either way, markets eventually find a way to recover.

For the disciplined long-term investor, market dislocations can provide significant opportunities – here’s how you can take advantage of them on Selfwealth by Syfe:

Anchor With Income: Don’t give up on the income opportunity. Bond yields (which rise when bond prices fall) are more attractive now.

Vanguard Global Aggregate Bond Index (Hedged) ETF (ASX: VBND) provides to a diversified portfolio of high-quality, income-generating securities issued by governments, government-owned entities, and investment-grade corporations from around the world. Available hedged to AUD, taking out currency risks.

BetaShares Australian Investment Grade Corporate Bond ETF (ASX: CRED) invests in a portfolio of senior, fixed-rate bonds issued by high-quality Australian corporations. It is offering equity-like income and could be well-positioned when interest rates eventually peak.

Spread Your Bets: Maintain a broad and globally diversified portfolio to capture the recovery – wherever it occurs.

Vanguard MSCI Index International Shares ETF (ASX: VGS) is a core holding for global diversification, providing exposure to over 1,000 of the world's largest companies across developed markets (excluding Australia).

VanEck MSCI International Quality ETF (ASX: QUAL) tracks a portfolio of highly profitable global companies across developed markets with strong fundamentals, low debt, and the pricing power needed to pass higher costs onto consumers without losing their margins.

Cash for Dry Powder: Stay flexible, preserve capital, and be ready to deploy when the moment comes for your high-convictrion bets.

Betashares Australian High Interest Cash ETF (ASX: AAA) aims to provide attractive, regular income distributions and a high level of capital security via cash held in Australian dollar interest-bearing bank deposit accounts.

iShares Enhanced Cash ETF (ASX: ISEC) invests in a highly liquid mix of short-term money market instruments and short-term corporate bonds, aiming to generate a slightly higher yield than standard bank deposit ETFs.

Finally, discipline matters: Keep dollar cost averaging (DCA), and use enhanced DCA – investing more than usual in significant sell-offs – to capture more of the opportunity.

We’ve integrated the Auto-Invest function directly into the new Selfwealth app and made it as simple as possible. Here’s how to get started:

Find your asset: Select a stock or ETF from your portfolio that you want to invest in regularly. While the popular options are listed above, the app also provides inspiration with easily surfaced insights and highlights of what is popular with our Selfwealth community.

Select 'Auto-Invest': Look for the Auto-Invest option within the order screen.

Choose your cadence: Align your trades with your pay cycle and select the frequency that works for you — weekly, fortnightly, or monthly.

Set the amount: Enter the dollar amount that fits your budget.

Once confirmed, the app will place Market Orders on your behalf at your chosen interval. You have full control to review, pause, or adjust your schedule at any time from your Portfolio or Orders tab.

Ready to automate? Update your Selfwealth app today to the latest version and head to the Auto-Invest section to get started.

Haven't downloaded the app yet?

Download today and stay connected to your portfolio anytime, anywhere.

Important disclaimer: SelfWealth Pty Ltd ABN 52 154 324 428 (“Selfwealth”) (AFSL 421789). The information contained on this website is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser and/or accountant. Taxation, legal and other matters referred to on this website are of a general nature only and should not be relied upon in place of appropriate professional advice. You should obtain the relevant Product Disclosure Statement for any product mentioned and consider its contents before making any decision.

Most Recent Articles