Key Takeaways

Many “safe havens” are failing as the Iran War drags on. Bonds, gold, and the yen are losing ground when investors need them most.

These assets work well during demand disruption but tend to falter in the kind of supply shock and inflationary threat confronted by markets right now.

Energy dependency is driving currency dynamics. USD is the one safe haven that’s still working, thanks to US energy independence and Fed rate expectations. Net exporter currencies (AUD, CAD) have fared better than net importers (e.g. JPY).

Income anchors performance. Despite the unsettling sell-off in bonds, income assets (REITs, bonds) benefit from the stability of regular payments. Yields have climbed to attractive levels. Many such assets have strong fundamentals.

Stay disciplined. Stay diversified. Now is a good time to review your portfolio and risk appetite. For most, simply staying invested, diversified, and dollar-cost averaging remains a sound strategy.

What are safe havens?

Safe havens are assets that are expected to hold their value or even appreciate when the broader market sells off. They are typically liquid (i.e. actively traded) and often tied to countries that are seen as stable. Examples include US Treasuries (i.e. government bonds), the Japanese yen, and the Swiss franc. Gold, a store of value for millennia, is the ultimate poster child.

Even in living memory, we have witnessed plenty of flights to safety. US Treasuries rallied at the outset of the Global Financial Crisis, and again at the outbreak of the Covid-19 pandemic. Gold’s multi-year rally was, arguably, sparked by the war in Ukraine and the geopolitical tensions that followed. The Swiss franc jumped against the euro at the start of that war.

How is this time different?

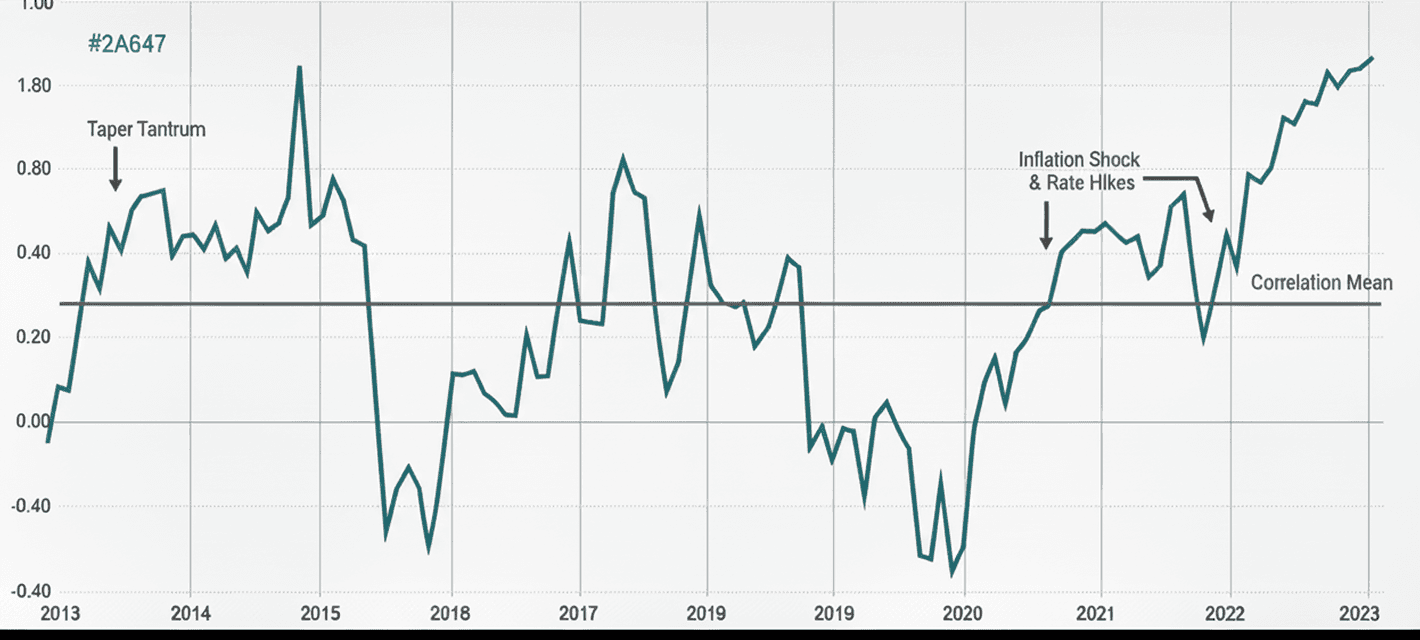

For the past four decades, many major crises followed the same script: growth collapsed, deflation loomed, central banks cut rates, and bonds rallied. Investors were accustomed to worrying first and foremost about demand destruction. This is not the case when supply disruptions dominate. An example would be 2022, when supply chain chaos sparked by the pandemic was compounded by the energy shock from the Ukraine War. In that case, bonds and stocks moved in the same direction, meaning bonds didn’t offer protection (see chart below).

A similar “supply shock” is unfolding now with the Iran War, which has caused the largest oil supply shock in recorded history. The Strait of Hormuz, through which 20% of global oil and liquified natural gas (LNG) supply normally transits, is effectively shut. Surging oil prices are already giving pause to those central banks about to cut interest rates. A protracted conflict could tilt them towards hiking. Some analysts fear the return of 1970s-style “stagflation”, with low growth, high inflation, and punitive financing costs all at the same time.

Source: LSEG. Chart shows the correlation of returns between FTSE Global All-World Index and FTSE World Government Bond Index.

Why exactly are safe havens not holding up?

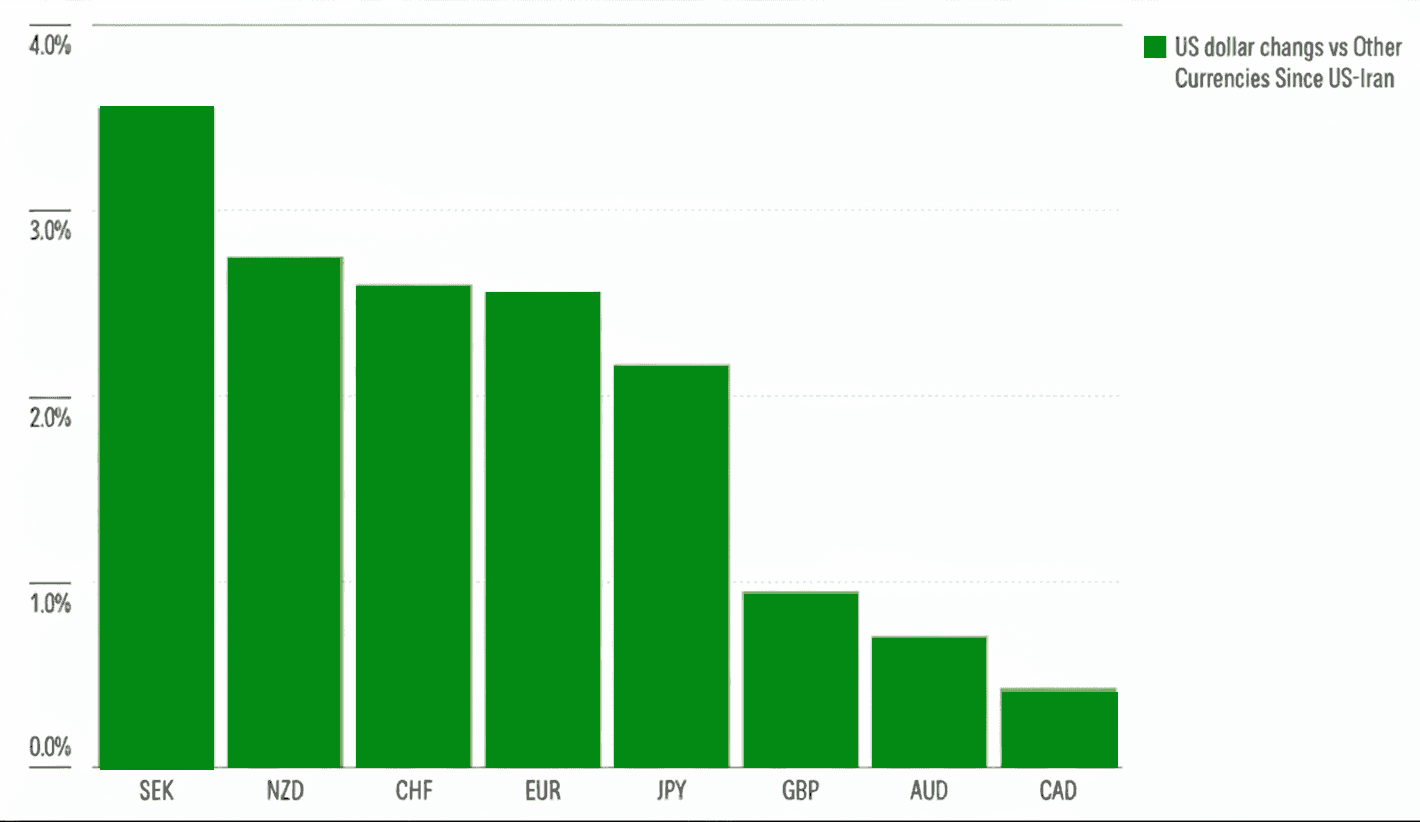

A couple of weeks into the Iran war, traditional safe haven assets have diverged. Bonds and gold have dropped, while the US dollar has rallied hard.

Currency markets are increasingly shaped by how dependent countries are on oil. US energy independence has proven to be a source of resilience. The dollar is also benefitting from shifting interest rate expectations, as markets now see the Fed keeping rates higher for longer.

Compare that with the yen, which has historically been a reliable haven. Its large trade surplus and vast overseas investment holdings mean that a lot of capital typically flows back to the Japanese currency during a crisis. That protection looks less convincing now that we have an oil crisis, with Japan being a big net oil importer.

The Aussie dollar and the Canadian dollar, both net energy exporter currencies, have held up better in the face of dollar strength, as shown in the chart below.

Source: Compiled by Morningstar based on Macrobond data, 17 March 2026.

Gold does not generate income, so when rates rise (or stay higher than markets had expected), bullion looks less attractive relative to bonds and cash. Given that gold has been a crowded trade (following an outstanding 80% rally over two years), some unwinding in a falling market is likely. In sharp sell-offs, leveraged investors are sometimes forced to liquidate positions to meet margin calls.

Because gold is priced in US dollars, a surging greenback also makes the yellow metal more expensive for non-USD buyers, dampening global demand and pushing prices down.

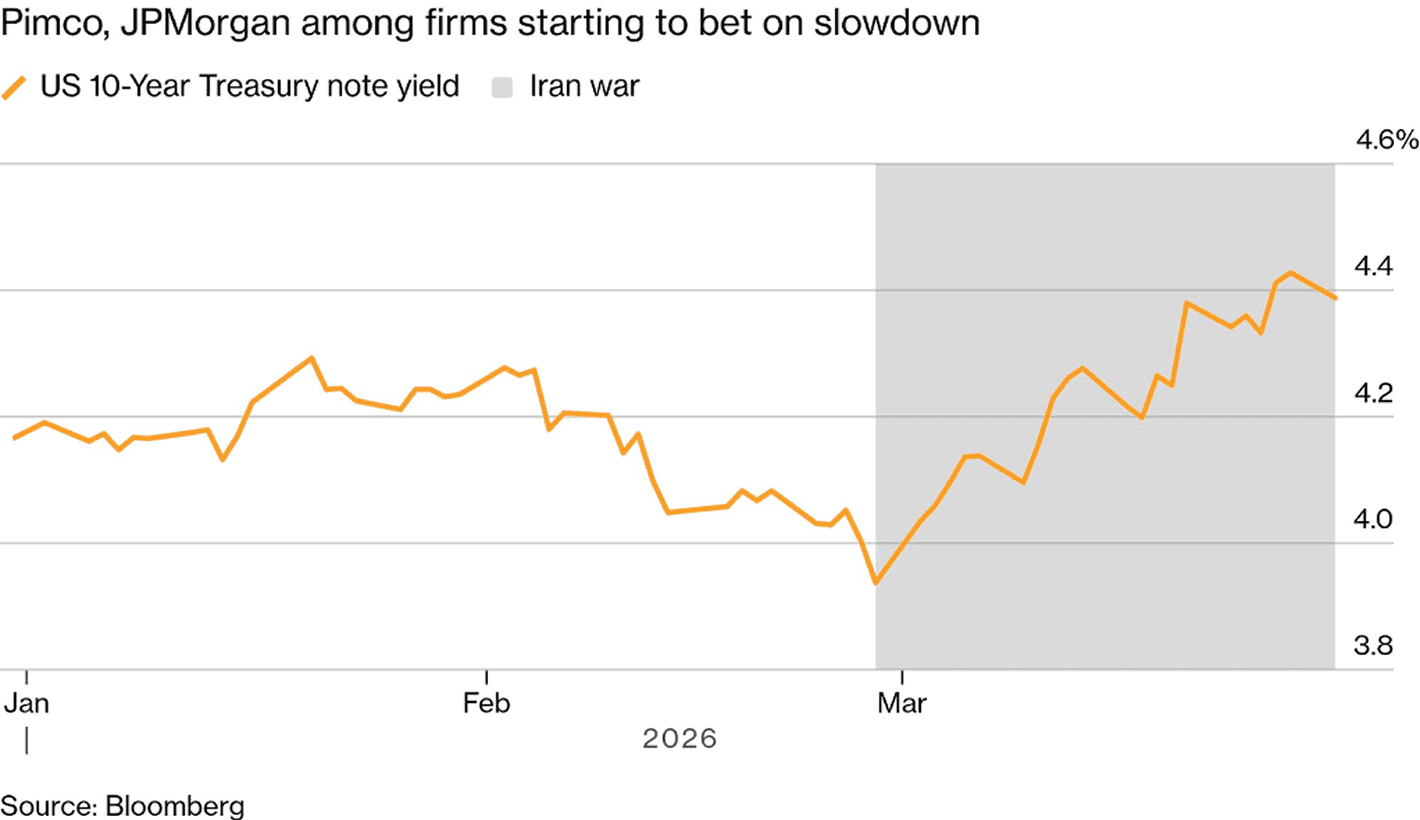

Bonds face a double whammy. At the short end of the US Treasury yield curve, traders are pushing up rates as they expect central banks to prioritise the fight against inflation (which they primarily do by raising near-term interest rates) over supporting growth. Bond’s prices and their yields have an inverse relationship: the lower the price, the higher the yield.

Long-dated bonds are faring not much better because markets see governments having to borrow and spend more in the long run, especially if the war drags on and inflicts lasting damage on the global economy. That means the risk for holding long-term bonds is rising, and bondholders want to be compensated for that.

A Word on Income: Anchoring Performance

The recent movements in fixed income can be unsettling, but it only presents half the picture. Total return in fixed income includes both capital appreciation and the coupons that are paid periodically to bondholders. These payments flow regardless of how much the underlying assets swing between now and their maturity date, serving as an anchor to portfolio performance.

With bonds selling off, their yields are also becoming more attractive. 10-year US Treasuries are offering yields well above 4%, prompting big institutions to turn more positive on bonds.

Where could markets be wrong?

Markets could be overestimating how high interest rates will rise. The economic fallout is less widespread now than in 2022, when a world reeling from the pandemic confronted both an energy crisis and supply chain disruptions. Right now, the crisis is mostly about energy.

Another point to note is that interest rates are already relatively high. This means, unlike a few years ago, central banks may have less room to hike because financial conditions become “restrictive” i.e. more than is needed to rein in price rises. Ramping up interest rates could risk triggering a recession.

Capital could move just as quickly in the other direction. Markets tend to rebound from conflicts once there’s a path to peace, even without a full resolution. That’s why wars generally have a short-lived impact on markets. Rate-sensitive assets could rally once that happens.

What to consider for your portfolio

To help navigate this environment, consider anchoring your portfolio by sticking to these key principles and potential investment options. For more detail on these ETFs, click the ticker codes below to view them in the Selfwealth app. If you don't have the app yet, scroll down and click to download.

Cash: Hold enough of it. Cash provides “liquidity” and flexibility, allowing you to preserve capital in a crisis, meet short-term spending needs, and accumulate ammunition to deploy when you see undervalued assets.

Betashares Australian High Interest Cash ETF (ASX: AAA) aims to provide attractive, regular income distributions and a high level of capital security via cash held in Australian dollar interest-bearing bank deposit accounts.

iShares Core Cash ETF (ASX: BILL) is an alternative to AAA that also invests in short-term money market instruments and bank deposits, providing high liquidity and capital preservation.

Ready for Income: Too much cash, however, would mean you’re forfeiting on higher-yielding income opportunities. Strike a balance. Hold enough cash during a crisis, but stand ready to pivot to higher-yielding income instruments.

Betashares Australian Bank Senior Floating Rate Bond ETF (ASX: QPON) aims to pay monthly income, exceeding the cash and short-term deposit rates, by tracking the performance of some of the largest and most liquid senior floating rate bonds issued by Australian banks.

Vanguard Global Aggregate Bond Index (Hedged) ETF (ASX: VBND) provides to a diversified portfolio of high-quality, income-generating securities issued by governments, government-owned entities, and investment-grade corporations from around the world. Available hedged to AUD, taking out currency risks.

Vanguard Australian Fixed Interest Index ETF (ASX: VAF) offers broad exposure to high-quality Australian government and corporate bonds.

Stay disciplined, stay diversified. The investors who fare best in more challenging markets are those who stay invested, disciplined, and diversified across asset classes, positioning themselves for the eventual recovery.

Vanguard MSCI Index International Shares ETF (ASX: VGS) is a core holding for global diversification, providing exposure to over 1,000 of the world's largest companies across developed markets (excluding Australia).

Betashares Australian Quality ETF (ASX: AQLT) aims to track a portfolio of 40 high-quality Australian companies. These companies are selected based on specific 'quality' metrics, including high return on equity (ROE), low leverage, and relative earnings stability.

Betashares Global Quality Leaders ETF (ASX: QLTY) provides access to 150 global companies (excluding Australia) that are ranked by the highest quality scores on a similar set of factors, including ROE and cash flow generation ability.

Review your portfolio. Volatile markets provide a reality check. Are your investment objectives really in line with your allocation? Do you have the risk appetite to stomach drawdowns and wait for the eventual rebound? Is your time horizon long enough to ride out the downturn, and do you need more cash out in the near-term?

These questions help determine if you can sleep well at night. For those answering yes, staying invested and “dollar cost averaging” is usually a pretty good strategy – and with Auto-invest available in the Selfwealth app, you have a simple way to stay consistent and in the market.

Haven't downloaded the app yet?

Download today and stay connected to your portfolio anytime, anywhere.

Important disclaimer: SelfWealth Pty Ltd ABN 52 154 324 428 (“Selfwealth”) (AFSL 421789). The information contained on this website is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser and/or accountant. Taxation, legal and other matters referred to on this website are of a general nature only and should not be relied upon in place of appropriate professional advice. You should obtain the relevant Product Disclosure Statement for any product mentioned and consider its contents before making any decision.

Most Recent Articles