As markets reacted positively to the news, oil prices fell, equities rose, and the US dollar slipped as bond yields fell. For Australian investors, the more durable story is what cheaper energy does to inflation — the single biggest constraint on central banks this year.

Key Takeaways

The US and Iran reached a deal to reopen the Strait of Hormuz, with a signing ceremony flagged for Friday and a 60-day window to negotiate sanctions relief and Iran's nuclear program

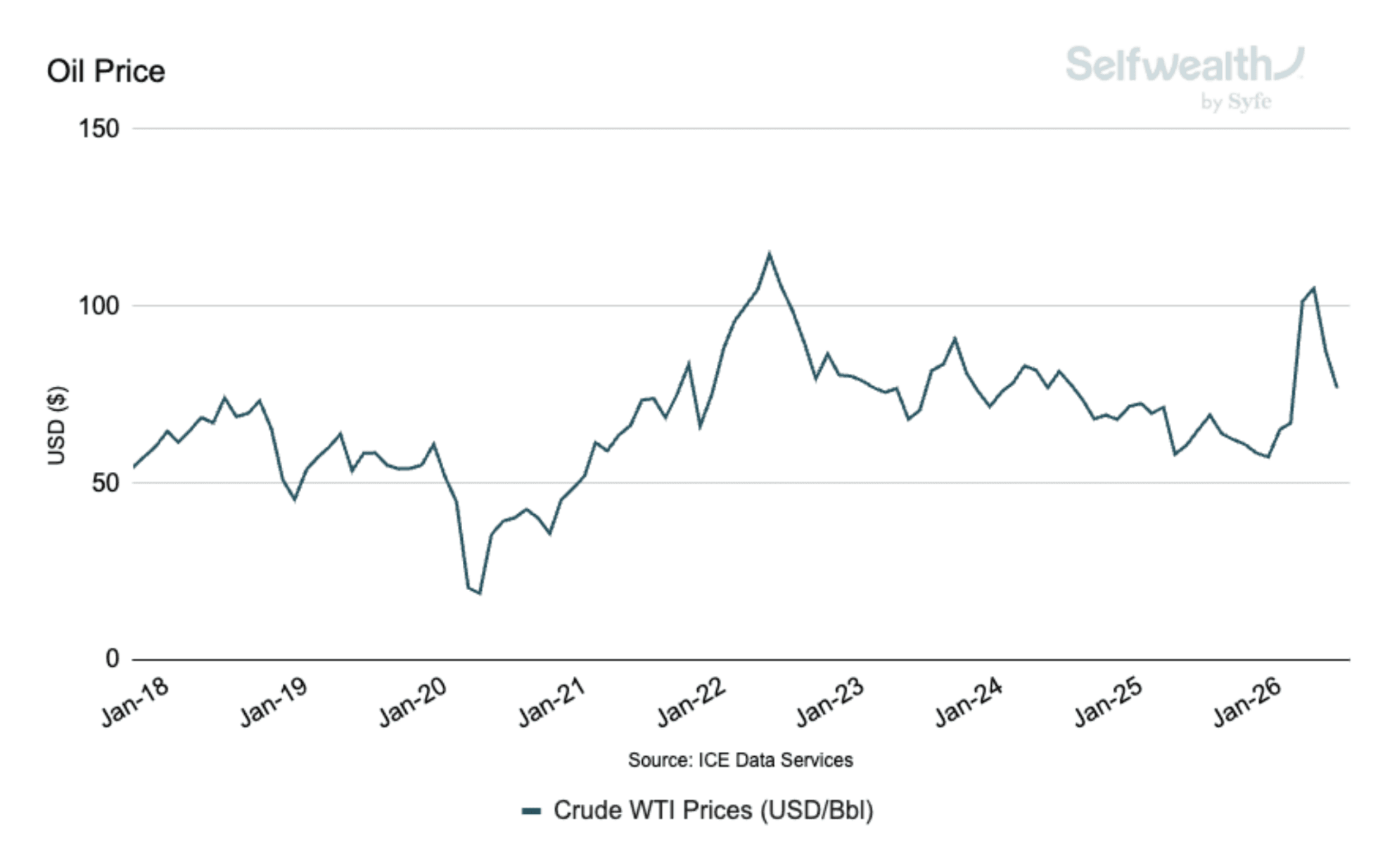

Oil prices fell on the news, down over 15% this month so far, unwinding a large portion of the premium built up during the war, while equities rallied and yields fell

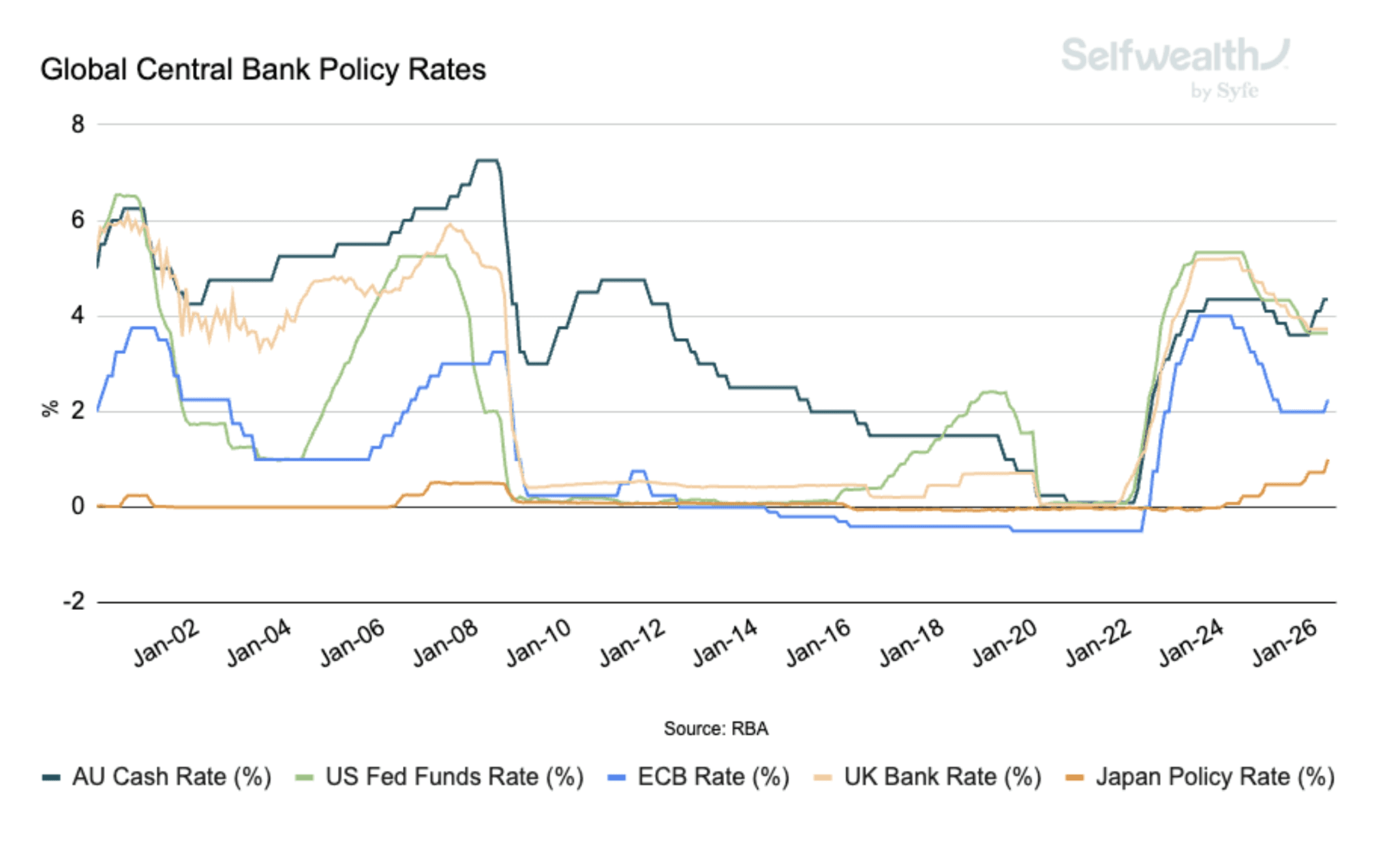

The RBA and the US Fed held rates unchanged this week, signalling inflation as the key watchpoint

The ECB and the Bank of Japan both hiked 25bps over the past week, to 2.25% and 1.00% respectively, tightening into an inflation impulse the Hormuz deal may now begin to unwind

The Gulf: Oil Prices ease on the back of potential deal

Over the weekend, the US and Iran reached a verbal agreement that provides for the toll-free reopening of the Strait of Hormuz, the removal of the US naval blockade, and an end to hostilities across all fronts, including Lebanon. A formal signing is expected in Switzerland on Friday, after which a 60-day negotiation begins on the detailed questions of sanctions relief and Iran's nuclear program.

On the news, oil prices fell closer to US$80 and have given back most of the war premium. Prices remain above pre-war levels but well below this year’s peak above US$120 a barrel. The full agreement text has not been released and a chance the deal does not hold, with any reopening likely to be fragile and slow. For Asia's energy importers and for Australian households squeezed by higher fuel prices, the direction of travel is a relief. For Energy sector stocks however, the fall in prices has led to underperformance recently.

Global Central Banks: Two Hold, Two Hike

Cheaper oil matters most for what it does to inflation. The fuel-price shock from the conflict had been feeding straight into the cost-of-living squeeze that drove Australian consumer sentiment to multi-decade lows.

Against that backdrop, the RBA and the Federal Reserve held interest rates steady this week, making clear they want to see how inflation evolves. A softer oil price buys them some breathing room in the short term, however, markets are still pricing in over 50% chance of a rate hike both for RBA and Federal Reserve by the end of the year.

Globally, the trend has still been for cash rates to rise. The ECB raised its key rates by 25 basis points last week, its first hike since 2023. The Bank of Japan followed with its own 25 basis points hike to 1.00%, moving its policy rate to the highest since 1995.

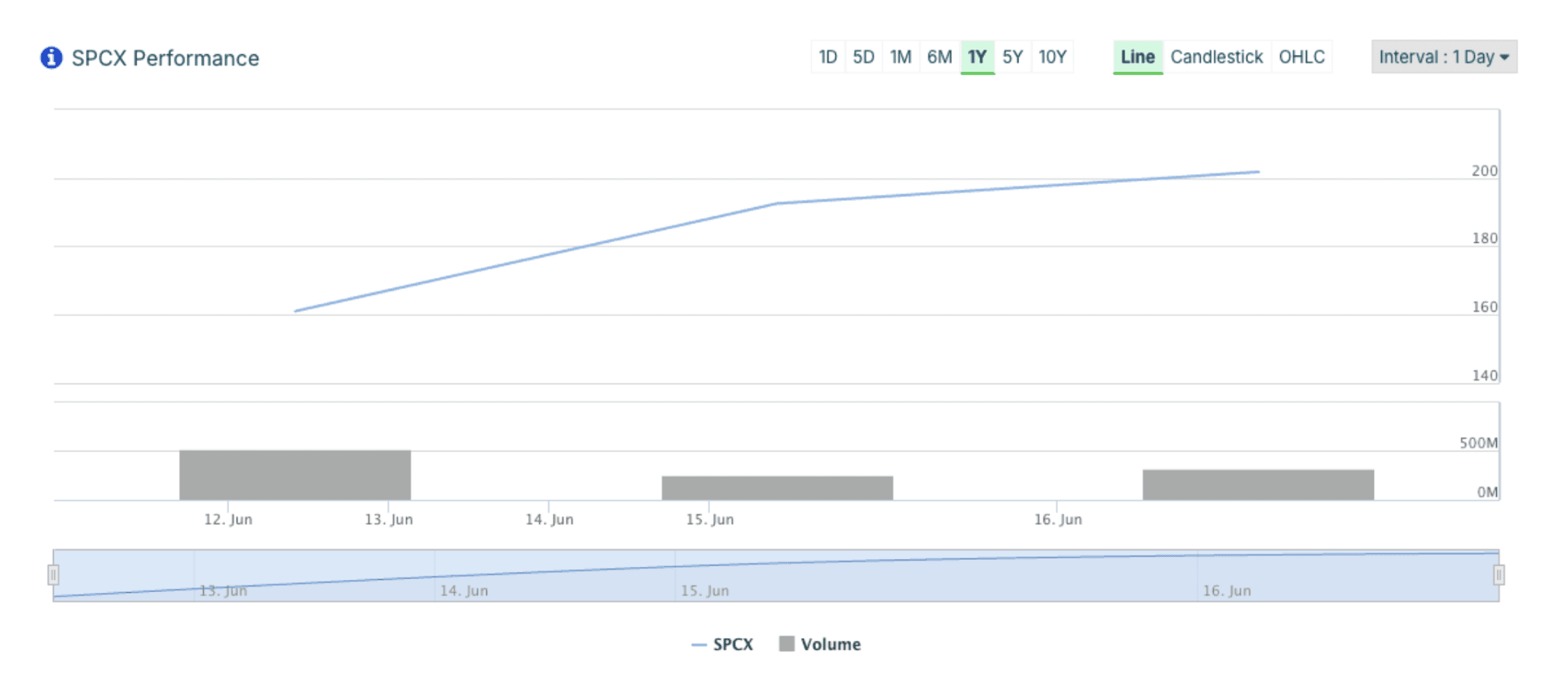

SpaceX delivered

The IPO we previewed last week landed with a bang. SpaceX's share price jumped 19% on its Nasdaq debut, valuing the company above US$2 trillion and making it the sixth-largest listed company in the US.

The broader signal is a healthy risk appetite, and a strong debut for the first of several AI-linked giants expected to test public markets this year, with Anthropic and OpenAI considering IPOs. However, there has also been some caution around the limited number of SpaceX shares available to trade, with long-term holders still in lock-up periods constraining supply, so early prices could be volatile as demand meets thin float.

Looking Ahead

The focus now shifts from the announcement to the follow-through: Friday's signing, whether ships actually start moving through Hormuz, and whether the ceasefire holds given Israel's stance. Domestically, Australian employment and inflation data next week will be the first meaningful read on the economy after this run of global events.

What We're Keeping an Eye on

Hormuz Signing — June 19: The formal signing is flagged for Friday in Switzerland. Watch whether it actually lands, whether the full agreement text is released, and whether tankers start transiting, as shipping-industry confidence remains low given the threat of mines, drones and missiles.

Ceasefire Follow-Through — ongoing: Israel and Hezbollah were still trading strikes in Lebanon, and Netanyahu said he and Trump "do not always see eye to eye" on the deal. Any re-escalation puts the oil premium straight back on.

Australian CPI (May) — June 24: The May monthly CPI is released on 24 June, the first inflation read since this run of global events. Note it largely predates the mid-June oil pullback, so elevated fuel costs will likely still weigh; the relief shows up in later prints.

Australian Jobs (May) — June 25: Labour Force data lands on 25 June. It feeds directly into the RBA's next call — a still-tight labour market reinforces the case for keeping rates high.

Important disclaimer: SelfWealth Pty Ltd ABN 52 154 324 428 (“Selfwealth”) (AFSL 421789). The information contained on this website is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser and/or accountant. Taxation, legal and other matters referred to on this website are of a general nature only and should not be relied upon in place of appropriate professional advice. You should obtain the relevant Product Disclosure Statement for any product mentioned and consider its contents before making any decision.

Most Recent Articles