Selfwealth

What Happened

The US and Israel attacked Iran over the weekend after negotiations broke down over the country’s nuclear programme, eliminating Iran’s leader and calling for regime change in Tehran. This signals a longer and broader campaign than previously thought. Iran has already retaliated against neighbouring Gulf states, beyond hitting US military bases in those countries.

Why This Matters for Markets

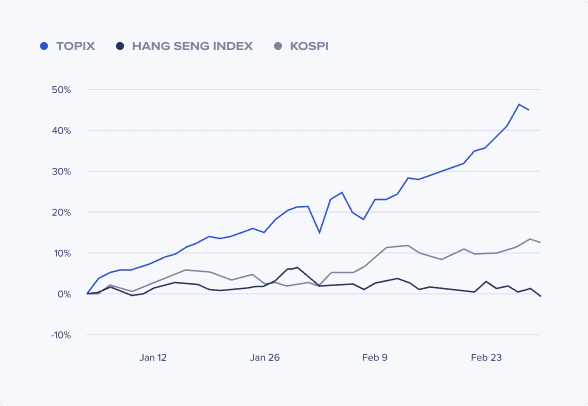

Markets opened on Monday with a risk-off move. Oil prices initially spiked over 10%, but they soon moderated to single-digit gains. Safe haven assets firmed — gold, the US dollar, and US Treasuries all had decent support in the Asian trading session. Equities slid, but only by around 1-2% in most cases. Developed Asia remains strong year-to-date, with outstanding gains in Japan and Korea, while Hong Kong is off marginally. This tells us that markets are pricing in concern, not catastrophe.

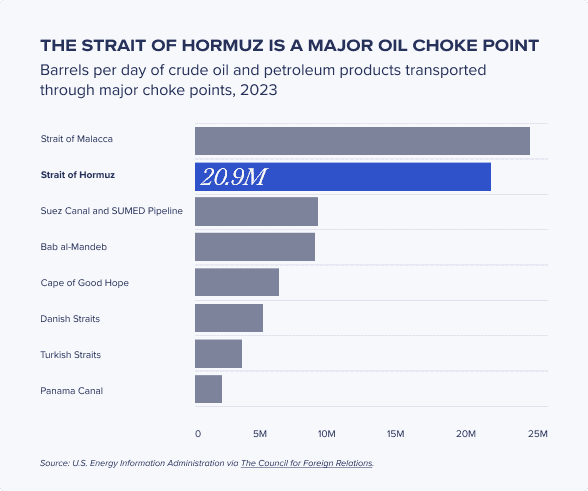

Sentiment could deteriorate, however, if Iran shuts the Strait of Hormuz for a prolonged period. This is a narrow stretch of water off its shores, through which 20% of oil and 30% of liquefied natural gas (LNG) globally is shipped. The country has leveraged the Strait as a bargaining chip before, in 2019 in response to US sanctions, and during the 1980s Iran-Iraq war.

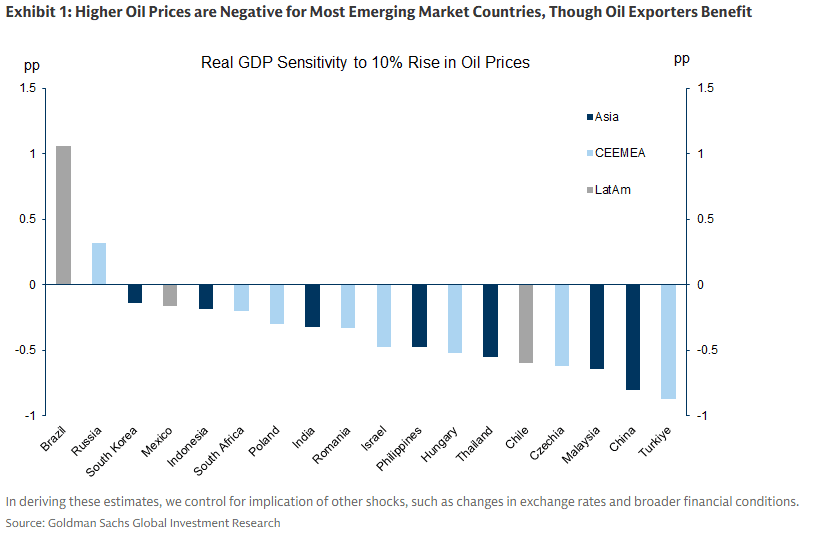

Major energy importers east of the region, China and India, are particularly vulnerable to shocks in this waterway. A 10% oil price increase would reduce real GDP in major oil-importing countries by up ot 0.8 percentage points, according to Goldman Sachs analysts.

A drawn-out conflict would have implications further afield, too. Europe’s energy prices could also be driven closer to levels at the start of the 2022 war in Ukraine. The most-feared (though in our view, unlikely) scenario is a rebound in US inflation, which would disrupt the Federal Reserve’s schedule for interest rate cuts. The stabilising global economy could be shaken.

Where the Bears Could Be Wrong

Some analysts fear a replay of the 1970s oil crisis, which also revolved around this part of the world, when supply disruptions sent the US economy into stagflation.

The Middle East, though important, is not the lynchpin it once was in the global energy network. Supply has been growing beyond the traditional OPEC group of oil-exporting countries. Accounting for other exporters in the broader “OPEC+” cohort, there is currently spare capacity. Supply is expected to outstrip demand in 2026, according to researchers at J.P. Morgan, who published their case shortly before the conflict broke out and projected softening oil prices this year.

Over in the US, energy independence has been on the rise. It is today a net exporter of oil and energy overall. Geopolitical tensions in and beyond the Middle East over the years have highlighted the urgency for many importing countries to diversify their sources of energy. In the case of a regime change in Iran, additional oil supply could be unlocked for global markets.

Where Do We Go From Here

Attacks have been escalating on both sides. With regime change now an explicit objective, neither side has much incentive to de-escalate quickly. Near-term, cyclical sectors and oil majors are most vulnerable to pullbacks. Markets will stay sensitive to news headlines.

That said, unless this broadens into a protracted regional war with severe and sustained oil disruption, the conflict is unlikely to be materially negative for global growth and become a meaningful risk for global equity markets.

Historically, the effects of military conflict on markets tend to be short-lived. According to LPL Financial, it takes on average 20 days for the S&P 500 index to bottom after a geopolitical crisis, and around 43 days (1.5 months) to recover.

Portfolio Implications: Discipline, Dispersion, Diversification

In many ways, the start of 2026 has been a continuation of 2025, defined by “dispersion” (i.e. the widening gap between winners and losers). What has changed is the intensity. Once-peripheral risks that have moved to the centre. Investors who are used to the “everything rally” and instinctive dip-buying need to adjust to a more disciplined and selective mindset.

Building for resilience through a broad portfolio should be a priority. In our 2026 outlook, we emphasised diversification as a driver of returns, not just a risk management tool, and recent events only strengthen our case. As the conflict unfolds, gold and US Treasury bonds are benefiting from safe-haven bids and providing a buffer for balanced portfolios.

For Australian investors, this means casting a wide net in and beyond the home market. Selection will be key in Australia as RBA hikes to fight inflation. Dispersion is already evident in the latest earnings season, with miners benefitting from the AI build-out and energy stocks outpacing consumer names. Further afield, global bonds offer income diversification where disinflation is already in motion, while emerging markets stand to benefit from relatively cheap valuations and once dollar weakness resumes. Asia’s AI ecosystem, from semiconductors in Taiwan and Korea to Chinese companies rivalling US AI giants, provides another path to build a broad portfolio that captures future growth outside of the concentrated US market.

Important disclaimer: SelfWealth Pty Ltd ABN 52 154 324 428 (“Selfwealth”) (AFSL 421789). The information contained on this website is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser and/or accountant. Taxation, legal and other matters referred to on this website are of a general nature only and should not be relied upon in place of appropriate professional advice. You should obtain the relevant Product Disclosure Statement for any product mentioned and consider its contents before making any decision.

Most Recent Articles